Retail market is looking to e-retailers and athleisure to drive leasing demand in 2021 says new research by Cushman & Wakefield

The Covid-19 pandemic has driven the prominence of online shopping and led to companies adopting or exploring flexible work arrangements. As such, we see e-retailers and athleisure brands to be significant in driving future retail demand. Amongst the malls that are due to be completed next year are Shaw Plaza (62,700 sf), One Holland Village (76,500 sf), 112 Katong (180,700 sf), all suburban malls

E-retailers who have thrived in the uptick in e-commerce may pursue a “clicks to bricks” strategy and take advantage of declining rents to open a physical store to gain more sales and brand recognition. For example, online fashion retailer, Love, Bonito opened their fourth store at Vivocity, occupying 4,300 sf. The athleisure trend is booming, driven by broad shifts in the choice of fashion as a result of flexible work arrangements and a greater focus on healthy and active living. Sportswear and Footwear retailer, Footlocker, has continued to expand and opened their sixth and largest store yet at Orchard Gateway @ Emerald, spanning 23,000 sf.

Christine Li, Cushman & Wakefield‘s Head of Research for Singapore and Southeast Asia, said: “Footlocker’s opening of its sixth store sends a strong signal that international brands are still on the hunt for quality real estate in Singapore, underscoring the city-state’s value as a launch pad to other neighbouring markets.”

There is still scope for brands to adopt a more aggressive online strategy to wean off a heavy reliance on foot traffic in physical stores. The retail landscape is challenged by the prolonged absence of tourists and social distancing measures inducing a reduction in capacity so it is imperative that retailers sharpen their focus on an online strategy that might expand their customer base beyond Singapore, for instance.

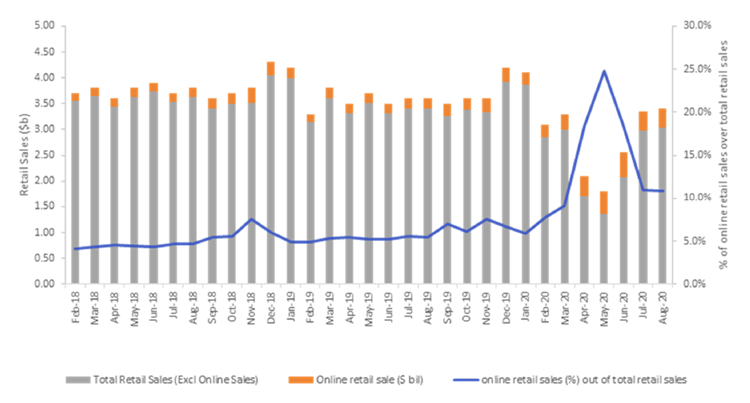

| Time Period | Proportion of online sales |

| 2018 | 5.0% |

| 2019 | 5.0% |

| Circuit Breaker Average | 20.6% |

| Post-Circuit Breaker | 11% |

Sources: Department of Statistics, Cushman & Wakefield Research

British fashion brands Topshop and Topman took the dive and closed their last Singapore outlet and shifted their business online and this might pave the way for others to follow suit.

Amidst weak economic conditions, prime retail rents fell across the board. Other City Areas ($20.25 psf/mo) and Orchard ($33,73 psf/mo) rents fell the most at 3.0 per cent and 2.9 per cent quarter-on-quarter respectively in Q3 2020, amidst the implementation of flexible working arrangements and on-going travel restrictions. Suburban prime rents ($30.85 psf/mo) were relatively more resilient and fell only 2.2 per cent from the previous quarter. Nonetheless, the spate of closures across the island will continue to put pressure on rent levels.

The retail operating conditions remain challenging, but first-tier malls have been able to hold on to their rental levels due to their high occupancy levels and ability to attract new tenants. On the other hand, weaker malls remain in distress.

Retail market going through dramatic transformation

Table of Contents

Mark Lampard, Cushman & Wakefield’s Executive Director and Head of Singapore Commercial Leasing and Regional Tenant Representation, said “The retail market is undergoing a dramatic transformation. In the short term, the easing of restrictions on people movement in Phase 3 is seen as a potential positive impact on retail sales, particularly at F&B outlets and other retail trades which had to stop operating abruptly because of the circuit breaker.

However in the longer term, the customer buying behaviour is likely to evolve with individuals seeking elements of both the online world such as instant product information, stock availability and product comparisons, and the real world where products and services are tried and tested before ultimately purchased.”

Cushman & Wakefield’s Retail Market Report in detail:

“Economy Lockdown

The Singapore economy contracted by 13.2% yoy in Q2 2020, marking the steepest drop in GDP historically. The plunge in GDP growth was due to the circuit breaker measures implemented, which saw the temporary closure of non-essential businesses. Against this backdrop, retail sales plunged by -35.3% qoq in Q2 2020, as consumers stayed at home and went online for their shopping needs. For the whole of 2020, the Ministry of Trade & Industry expects the GDP growth to fall by -7.0% to -5.0%, the largest economic contraction since Singapore’s independence in 1965.

E-retailers and Athleisure to Grow

The Covid-19 pandemic has driven the prominence of online shopping and led to companies adopting or exploring flexible work arrangements. As such, we see e-retailers and athleisure brands to be significant in driving future retail demand. Some e-retailers which have thrived due to the rise in e-commerce, may pursue a “clicks to bricks” strategy and take advantage of declining rents to open a physical store to gain more sales and brand recognition. For example, online fashion retailer, Love, Bonito opened her fourth store at Vivocity, occupying 4,300 sf. The athleisure trend is booming driven by broad shifts in the clothes people are wearing due to flexible work arrangements and a greater focus on healthy and active living. Sportswear and Footwear retailer, Footlocker, has continued to expand, and opened her sixth and largest store yet at Orchard Gateway @ Emerald, spanning 23,000 sf.

Market Conditions Remain Challenging

Amidst weak economic conditions, prime retail rents fell across the board. Other City Areas ($20.25 psf/mo) and Orchard ($33.73 psf/mo) rents fell the most at 3.0% and 2.9% qoq respectively in Q3 2020, amidst the implementation of flexible working arrangements and on-going travel restrictions. Supported by nearby residential catchments, suburban ($30.85 psf/mo) prime rents were relatively more resilient and fell only 2.2% qoq. Nonetheless, the spate of closures across the island will continue to put pressure on rent levels. For example, British fashion brands Topshop and Topman have closed their last Singapore outlet, and shifted their business online. The retail operating conditions remain challenging, but first-tier malls have been able to hold on to their rental levels due to their high occupancy levels and ability to attract new tenants. On the other hand, weaker malls remain in distress.”