As payments are bundled together with other services and consumers expect them to be costless (or free cash movement).

By: Hitesh Khan/

But with the free cash movement banks and retailers need to rethink their strategy:

- The nature of payments is changing quickly with technology advances and the rise of e-wallets.

- The payments function increasingly is embedded as just one feature among many—for example, in a mobile app—where the core value and profit derive from other services.

- This phenomenon has accelerated the most in Asia, where consumers have leapfrogged over card payments to adopt e-wallets, notably in super-apps such as WeChat.

- Banks, card companies, retailers, telecommunications firms and technology firms all should assess what role payments will play in their proposition to merchants or consumers.

Payments are having their moment in the limelight as technological advances and the rise of e-wallets and open banking continue to redefine customer expectations. While this phenomenon is most prominent in Asia, the rest of the world is primed to follow suit. Banks, retailers and others who are used to making money from payments need to rethink their strategy now.

“The monetary authorities of Singapore, the Philippines and Thailand envision that situation even for cross-border payments. In India, the early successes of the “India Stack” unified software platform and the Unified Payment Interface (UPI) real-time payment system are being studied by other governments as a potential model to make national payment systems more accessible and efficient. The Indian government is also considering abolishing the “merchant discount rate” charges on merchants who allow their customers to make payments through “low-cost digital payment modes.””

How can providers adapt quickly to the idea of free cash?

How can providers adapt quickly to the idea of free cash?

This is the key takeaway from Bain & Company’s new report, Payments Just Want to be “Free” –How can Providers Adapt?, published ahead of Sibos 2019 in London.

“Payments are at the forefront like never before,” said Thomas Olsen, a partner with Bain & Company’s Financial Services practice and a co-author of the report. “What’s happening now in Asia foreshadows the types of developments that could soon occur everywhere else. The experience is simple and seamless, and increasingly innovative providers keep raising the bar when it comes to what consumers and merchants expect.”

Traditional players who do not adopt the concept of free cash will suffer

The profit pool for traditional players that do not adapt will suffer. Thus, companies across industries – banks, retailers, and tech platforms, for example – need to rethink their strategy now.

Some strategic options for existing payments providers include:

- Consolidating through mergers and acquisitions, in order to become more efficient in processing and innovation, enter new geographies or business segments, and to expand their opportunities for cross selling

- Adding services beyond traditional terminals and transaction processing, such as lending to merchants and consumers, and business management software that includes payroll, inventory and customer relationship management

- Facilitating e-commerce transactions and integrating payments with the store register.

Future view of free cash

“The future view of payments is increasingly clear: free, easy and embedded into other products and services,” said Glen Williams, head of Bain & Company’s global

Payments practice. “A critical mass of consumers will soon demand ‘invisible payments’ at most places they shop, so retailers should start thinking now about what this means for them.”

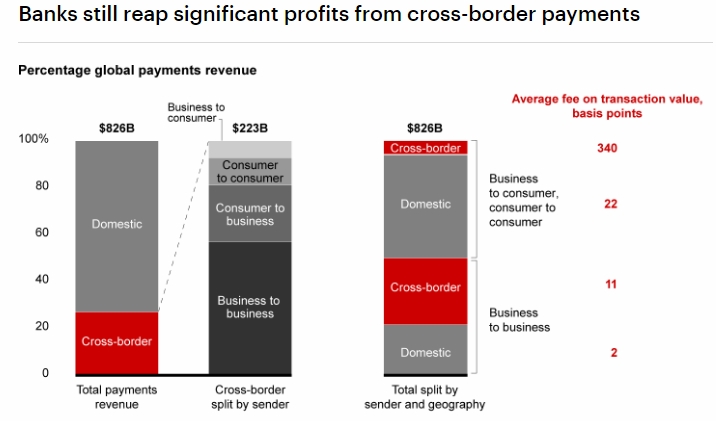

“Some mobile apps, such as GrabPay, already offer payments solutions to both consumers and retailers for nothing, using payments as a tool for rapid customer acquisition and leveraging the data to monetize other services. Even in mature card markets where payments remains profitable for banks, merchant acquirers and gateway or payment service providers, including the US, parts of Europe, Brazil and Australia, profits from standalone payments are under pressure and pricing will inevitably decline.”

Banking sector will be affected by this free cash concept as well

The banking sector will also be to be affected by the changes in payments, and banks will have to decide which of their current profit pools they cede in order to stay relevant.

“The innovation in payments is moving at a breakneck pace – and anyone who is currently making money from payments needs to think about how to broaden their offering into additional business lines to ensure that they maintain profit levels in the future,” said Mr. Williams. “The winners will be those who define clear choices and take action to redefine themselves and solidify their place in this new and exciting payments ecosystem.”

“Banks will need to decide which of their current profit pools they cede in order to stay relevant in the future payment world. They will also have to evaluate technology choices for modernizing payment capabilities.”

Mr Paul Ho, chief mortgage officer at iCompareLoan, said, “the free cash movement is already affecting many sectors, including the real estate market, and it is crossing traditional borders.” He added, “e-wallets are making transactions between parties much easier.”

Electronic payments (e-payments) have been around for many years, from the introduction of GIRO in 1984, to FAST and e-wallets for mobile phones today. E-payments are a convenient alternative to the use of cash and cheques as payment modes. They offer consumers a swift and efficient way to pay, and help businesses to enhance productivity.

The Singapore Parliament passed the new Payment Services Act (PS Act) in January 2019 to unify and streamline the regulatory requirements for various payment services in Singapore, including e-payments. The PS Act adopts a modular and risk-focused approach to tailor MAS’ rules according the scope and risks of each payment service. This gives MAS the flexibility to respond quickly to the fast changing payments landscape, and preserves stability while facilitating the innovation and growth of e-payments in Singapore.