The local residential property market thrived in Q3 2020 despite the pandemic and economic uncertainties. The sector emerged from the lacklustre performance in Q2 2020 and put up a commendable showing in Q3 2020, as strong local end-user demand for homes underpinned sales and supported prices in both the private residential and public housing segments.

While buying interest in the local residential property market remains keen, the recent clampdown on the re-issue of Options to Purchase (OTPs) by the authorities could likely temper new home sales volumes in the final quarter of 2020.

Nevertheless, transaction volume in the local residential property market for full-year 2020 is still expected to be strong, a remarkable outcome for a year hit by the COVID-19 pandemic.

Private Residential Property

Overall private home prices in Singapore rose by 0.8% in Q3 2020, unchanged from the flash estimate released earlier this month. This marked the second straight quarter of price increase following the 0.3% growth posted in the previous quarter, according to the latest real estate statistics announced by the Urban Redevelopment Authority (URA). Taken together, the URA Property Price Index has risen by 0.1% in the first nine months of 2020 from end-2019.

The Landed Property segment led the price increase in Q3 2020 where home values rose by 3.7% from Q2 to Q3 2020 – driven by stronger demand for landed homes during the quarter. Based on Realis data, there were 599 landed home transactions in Q3, up by 183.9% from 211 deals in Q2 2020.

Meanwhile, Non-Landed Property prices inched up by 0.1% quarter-on-quarter (QoQ) in Q3 2020, supported by firmer prices in the Rest of Central Region (RCR) and Outside Central Region (OCR). Home prices in the RCR increased by 2.5% QoQ in Q3 2020 as several new projects launched in this sub-market – including Forett At Bukit Timah, Penrose, Verdale, Noma, and Myra – helped to support values. In the OCR, non-landed home prices climbed by 1.7% QoQ as healthy demand for homes from local end-user and HDB upgraders continued to drive sales in this market segment. Notably, the OCR private residential property index, with a reading of 180.4 in Q3 2020, has hit a new peak last quarter.

Bucking the uptrend, home prices in the Core Central Region (CCR) fell by 3.8% QoQ in Q3 2020, with home values likely dragged lower by softer home prices in the resale market as well as continued travel restrictions which has crimped foreign buying.

Ismail Gafoor, CEO of PropNex, commenting on the local residential property market said: “Notably, in the primary market, Singaporeans and HDB upgraders continue to underpin new home sales, accounting for about 81% of the purchase in Q3 2020.”

“This could suggest that many Singaporeans are still confident about their job security – partly helped by the various government support packages – or that many households are still flushed with liquidity and have decided to enter the property market when they see good value. Looking at the first nine months of this year, nearly 80% of new private homes sold were bought by Singaporeans – representing the highest proportion since 2010, according to Realis data.

Other possible reasons for the strong sales could be buyers’ confidence in Singapore’s gradual economic recovery and re-opening of the economy as the country progressively finds a path towards the new normal. We remain positive about private home sales this year. Having said that, we think new home sales activity could moderate in the final quarter of 2020. Based on market observations, while home buying interest remains keen, the recent clampdown on the re-issue of OTPs is likely to dampen sales slightly in the months ahead.

A total of 13,980 private homes have been sold in the first nine months of 2020. Supported by a healthy demand in the resale market, we expect overall sales in 2020 to possibly hit 19,500, exceeding the 19,150 units transacted in 2019. We anticipate overall private home prices to remain resilient, potentially rising by up to 1% for the whole of 2020. Several factors such as the benign interest rate environment, debt moratorium programme, and support measures to preserve jobs have also strengthened holding power among home owners and helped to keep prices stable.

With unsold inventory declining to 26,483 units as at the end of Q3 2020 – down from the 36,839 units in Q1 2019 – we believe developers have a sufficient runway to sell units within the stipulated 5-year additional buyer’s stamp duty (ABSD) timeframe.”

HDB Resale

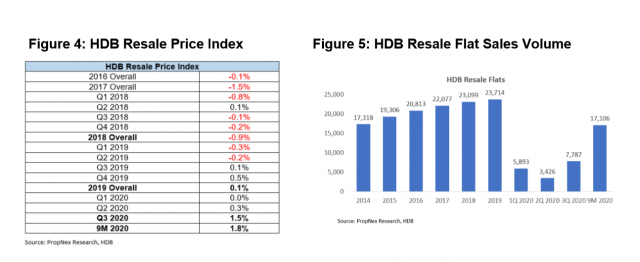

The Housing and Development Board (HDB) has also released its HDB Resale Price Index which showed that resale prices of public housing flats rose by 1.5% in Q3 2020, building on the price stability witnessed in the past year. The 1.5% print is also marginally higher than the 1.4% growth indicated in the flash estimate announced on 1 October 2020. For the first nine months of 2020, HDB Resale Price Index has increased by 1.8% from the end of 2019.

In Q3 2020, 7,787 HDB resale flats changed hands, marking the highest quarterly sales in 10 years, since 8,205 flats were resold in Q3 2010, based on data tracked by PropNex Research. The Q3 sales took total HDB resale volume to 17,106 units in the first nine months of 2020.

Wong Siew Ying, Head of Research and Content at PropNex, commenting on the local residential property market said: “The 1.5% increase in HDB resale prices in Q3 2020 marks the largest quarterly increase in resale flat values in more than seven years, since the 1.3% growth recorded in Q1 2013.”

“This can be seen as a milestone in the journey toward recovery for the HDB resale segment, where prices have been relatively soft since the implementation of the 30% Mortgage Servicing Ratio in 2013.

In all likelihood HDB resale values in 2020 will outperform the 0.1% increase posted in 2019. We are projecting HDB resale prices to rise by 2.5% to 3% in 2020, possibly marking the fastest pace of price increase since the 6.5% growth in 2012.

The brisk sales observed in Q3 2020 were likely fuelled by several factors, including the new housing grant announced last September – which provides up to $160,000 in grants for resale flat purchase by first-timer families – continuing to gain traction among buyers. In addition, the delay in the completion of some new flats due to construction disruption likely diverted some buyers to the resale market. Amid the uncertain economic outlook, it is also possible that some buyers went for a more affordable housing option in the HDB resale market, rather than buying a private home. We expect the sales momentum to continue in Q4 2020, potentially pushing total HDB resale volume to well above the 23,000-mark for the whole of this year.

We note that there are an estimated 24,163 HDB flats reaching the Minimum Occupation Period (MOP) in 2020 and another 25,530 flats in 2021 which will make them eligible to be resold. As the HDB resale market recovers, some HDB owners may be encouraged to upgrade from public housing to a private residential property. We think this potential pool of upgraders and the firmer HDB resale prices would act as a base and help to provide support to the private residential market.”