Millennial property consumers will play a major role in influencing investors and occupiers’ real estate decisions

Launched today at CBRE Symposium: The Singapore Journey, CBRE’s flagship thought leadership offering, Real Estate 2030 – Singapore, examines how our living and work spaces will transform over the next 10 years, driven by five major structural changes – demographics, infrastructure, occupier trends, sustainability and technology. The report explores how these changes will impact real estate investors and occupiers who will have to stay nimble and start preparing for these fundamental shifts.

Mr Moray Armstrong, Managing Director of CBRE Singapore, said, “The Singapore government continues to demonstrate vision and creativity in its approach to urban planning. This is fundamental to supporting long term economic growth, developing new growth areas and sectors, while helping to transform existing industries. Real estate investors and occupiers will face rapid changes in the market over the next decade. Changing demographics, infrastructure investment and technology advancements will present both challenges and opportunities for real estate players.”

Millennial property consumers are defined loosely as those born between the early 1980s to the mid 1990s, are projected to form the largest consumer group in Singapore by 2030, as they reach their prime working and spending years.

Table of Contents

Mr Desmond Sim, Head of Research, Southeast Asia, CBRE, commented, “While technological innovations have continuously redefined the real estate landscape, by 2030, millennials will also play a major role influencing investors and occupiers’ real estate decisions. They will be the driving force behind the sharing economy where co-living and co-working are expected to be prevalent. Meanwhile, there will be more decentralized office stock; and in 10 years’ time, occupiers will have to adopt workplace strategies to cater to a five-generation workforce.”

Report highlights:

1. Demographics shifts to affect the fundamental demand for real estate

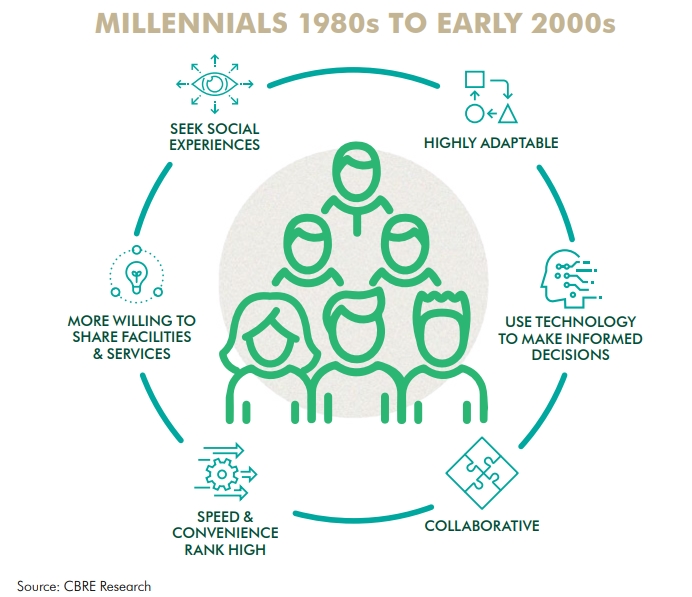

Millennial property consumers possess a particular set of values which are unique from other generations; one of these is the ability to be highly adaptive and more willing to share facilities and services.

- Home sizes for private housing have been declining – from 103 square meters in 2008 to 70 square meters in 2018. This is partly due to rising land costs which have induced developers to reduce unit sizes in a bid to keep overall prices affordable.

- Nonetheless, this may not necessarily translate to smaller living space per person due to shrinking household sizes, lifestyle changes, digitization and better space optimization. Living space per person has remained at about 28 square meters based on an average five-room HDB flat for the past two decades.

- Given that Singapore’s population is greying at a faster pace than a decade ago, there are schemes to help the elderly plan for retirement. This, in turn, could result in more residential sites of shorter tenures which would provide buyers and developers with more options.

- Millennial property consumers, who will form the largest consumer group by 2030, are highly adaptative, more willing to share facilities and services, and place more importance in seeking experiences. They will help drive the sharing economy and influence how developers and landlords make decisions.

Millennial property consumers also place more importance in seeking experiences, influencing how retailers and landlords shape the shopping experience.

2. Infrastructure to pave the way for growth

- Satellite strategic gateways (Jurong Innovation District, Punggol Digital District, Agri-Food Innovation Park, Changi Aviation Park and Tuas Mega Port) which possess their own unique propositions will encourage commercial growth outside the city and help to support innovation in various niche industries such as high-tech manufacturing.

- Infrastructure, such as storage facilities, if moved underground, can free up extensive tracts of land. Singapore has made good progress in tapping underground spaces and such space exploration will continue in the future to ensure that as more areas are freed up, land plots of higher value are preserved.

- Two current major challenges pertaining to the last mile in Singapore are unconsolidated deliveries and high delivery failure rates. The future of retail could see fulfilment centres moving closer to homes, increasing the overall efficacy of last-mile delivery. One viable option is for fulfilment centres to be located in residential precincts (for example, Marsiling, Aljunied and Ang Mo Kio), given the availability of industrial land parcels in these areas.

- Guided by the 20-minute town and 45-minute city vision, the expansion of the MRT network will result in increased connectivity, resulting in the narrowing of real estate premiums between the central and fringe areas.

Millennial property consumers will help to drive the sharing economy and influence how developers and landlords make decisions.

3. Occupier trends that will shape Singapore real estate in 2030

- Decentralization efforts are set to continue on a larger and wider scale, supported by improvement in infrastructure and accessibility. The portion of decentralised offices has grown from 17% in 1998 to 24% of total islandwide stock as of end 2018. This is expected to increase to 30% by 2030.

- There will be a wider acceptance of the sharing economy which will result in an asset light society. Each car sharing could reduce the number of vehicles by an estimated four cars, which could also reduce up to 15%-20% of building space previously used for roads and parking. The rise of co-living will also reduce the demand for three additional housing units for every home share.

- As at June 2019, approximately two in five of all office buildings tracked by CBRE Research has some flexible office component. By 2030, at least three out of five such buildings will have a flexible office component.

- Technology will be more widely used to create a convenient and seamless in-store retail experience. By 2030, stores will likely be equipped with artificial intelligence, sensors, self check-out stations, cameras and mobile devices. All items will have a RFID tag which can provide real-time inventory information to retailers who can then better manage inventory and reduce the amount of space needed for in-store warehousing.

- Co-retailing, which offers shareable spaces and community-based experiences between retailers and customers, will be on the rise. This will benefit entrepreneurs and start-ups who have smaller size requirements and may not be able to afford prime retail spaces.

- By 2030, Singapore will see a five-generation or 5G workforce comprising baby boomers, Generation X, Millennials, Generation Z and Post-Generation Z. Occupiers will have to strike a balance in their workplace strategies to meet the differing needs of these generations.

4. Sustainability continues to be a growing part of corporate agendas

- According to the Building and Construction Authority, it is expected that at least 80% of buildings (gross floor area) will be certified green. Some developers have pushed out green leases where landlords share energy consumption data with tenants, with the aim of achieving a lower energy consumption rate collectively. While such green leases are not yet prevalent today, CBRE expects such leases to be more common by 2030.

- Property developers are increasingly looking towards green financing as an additional source of capital. This includes any form of financing linked to environmental, social and corporate governance metrics such as green bonds, green loans and sustainability-linked loans.

- Driven by the state’s ’30-by-30’ vision to produce 30% of our food locally by 2030, developers will realise the value of converting under-used or alternative spaces for food gardening; urban farming will eventually be integrated into real estate.

5. Technology will be integral to the built environment

- On the back of widespread adoption and pervasiveness of cloud technologies, companies no longer need space for servers nor maintenance staff onsite. This reduces the need for commercial spaces, while increasing the demand for data centres as cloud storage.

- The rollout of 5G in Singapore will provide economic growth drivers by enhancing what industries can do with mobile connectivity, as well as give significant competitive advantages for applications with high bandwidth requirements. Specific to real estate, improved connectivity will help facilitate

communication between teams and promote flexible or remote working. - As the amount of big data increases, data storage and computing power facilities will have to keep up. However, with the introduction of stronger networks like 5G, data will increasingly be propagated from data centres and the cloud into mobile or edge devices. This trend, known as edge AI, will enable real-time decision making for applications such as autonomous logistics and predictive maintenance.