P2P loan or most commonly referred to as Peer-t0-peer loan, this may be alien to you. Most of you are familiar with home loan, car loan and personal loan. But what about P2P loan and bridging loan? P2P loan is quite a new type of loan in the market while bridging loan is less talked about compared to home loan. It is no wonder why people are less familiar with them.

To help our readers make more shrewd financial decisions, the iCompareLoan team feels that it is important for you to learn about P2P loan and bridging loan, especially the latter. (P.S. You might even use it one day when you are thinking of buying your second property). Thus, we created this guide on P2P loan and bridging loan. This guide will help you understand the mechanics of P2P loan and bridging loan. It will also help you to differentiate between the two.

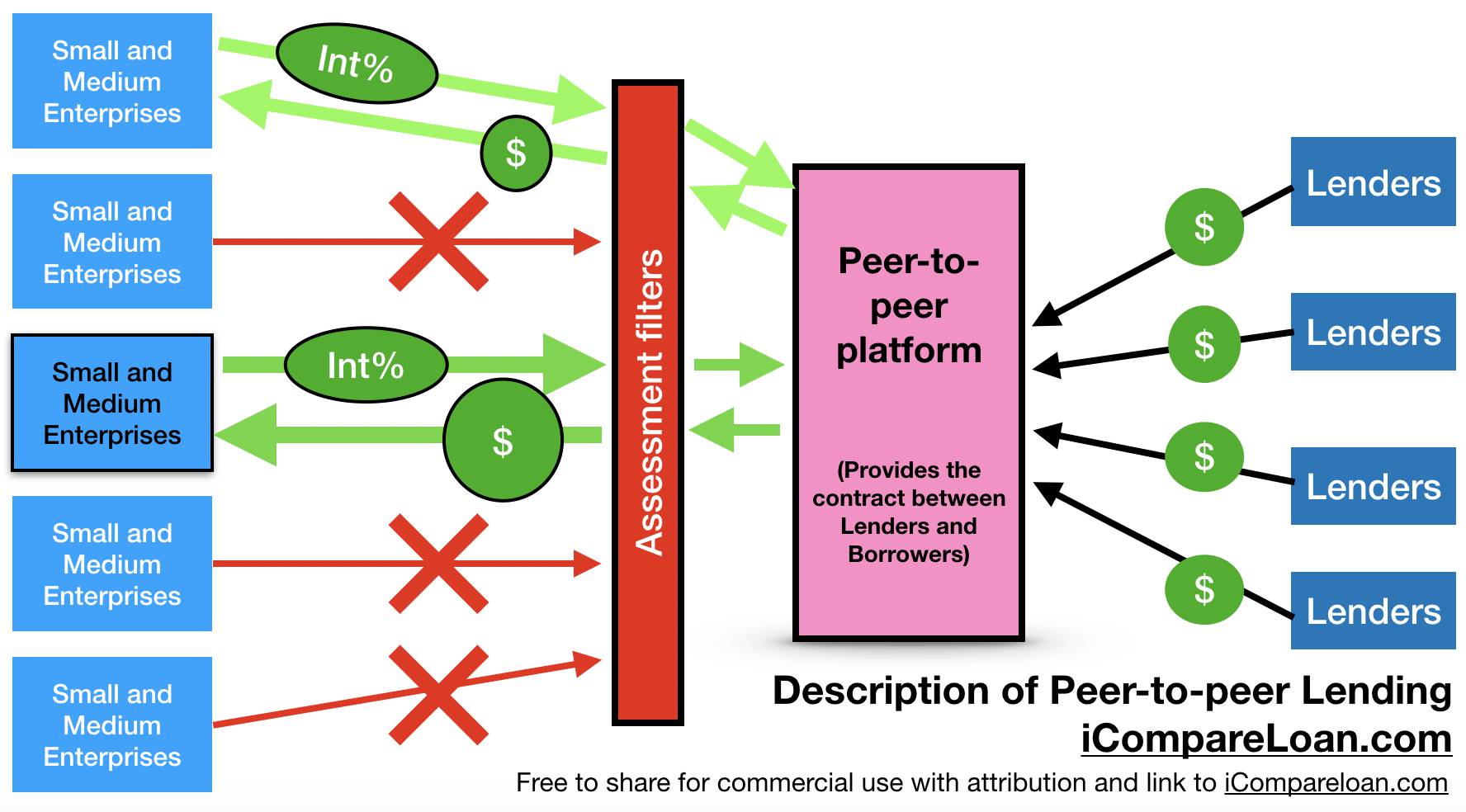

Picture: Description of peer-to-peer lending

1. P2P Loan

What Is P2P Loan?

Table of Contents

P2P loan, or Peer To Peer loan, is a type of loan that is borrowed from individuals instead of the usual banks or financial companies. So, instead of owing money to the bank or financial company, the borrower will be indebted to an individual/a group of individuals who have offered to borrow money to the borrower.

Contact the guys at iCompareLoan.com/contact who can walk you through the complexities.

How Does P2P Loan Work?

Since P2P loan involves multiple individuals extending loans to each other, a central marketplace is required to facilitate the lending activities. Borrowers, typically small and medium businesses (SMEs), will go to P2P platforms like Funding Societies, Minterest, MoolahSense and CapitalMatch, to request for funding. Public investors who are willing and able to lend money to these SMEs will also go to P2P platforms to find lending opportunities.

In return for extending credit to the SMEs, the investors will receive interest on their loan. This is just like how banks earn interest by lending money to you when you buy a house.

3 Types Of P2P Loan Products

While P2P loan is one type of loan, it consists of three different categories of loans. These three categories of loans are: Invoice financing; Business/Term financing and Property-backed financing.

1. Invoice Financing

When SMEs buy and sell goods and services from each other, they typically adopt a credit system. Unlike consumer transactions, transactions between businesses typically takes a few months for processing. It is common for companies to use a 30 to 90-day credit period instead of demanding their customer pay cash up front.

However, this can lead to a cashflow problem for companies, especially if the payment term they offer differs from their supplier’s payment term. Just imagine if all your customers take 90 days to pay you back but your supplier wants you to pay them in 30 days. You won’t have enough cash to meet the liability to your supplier.

This is where invoice financing helps SMEs. Once you have delivered goods or services to your customer, an invoice will be issued. Let’s say the invoice has a 90-day credit period, but you need cash to pay your supplier in 30 days. Here’s what you do. You use the invoice as a collateral to get capital from P2P platform. P2P investors will give you cash up front. In return, they will get earn some interest once the invoice is paid up by your customer.

Typical Characteristics of Invoice Financing

| Characteristic | Typical Range |

| Financing Amount | 70 – 90% of invoice value |

| Financing Duration | 15 days – 1 year |

| Annualised Interest Rates | 6 – 20% |

| Success Fee | 2 – 5% |

| Revenue Requirement | S$100,000 – S$500,000 |

| Cash Disbursement | 3 days – 1 month |

2. Business/Term Financing

Business/Term financing is a loan taken by SMEs for the purpose of expansion. For example, if the mamashop at your void deck wants to open a new shop in another area, the owner will apply for a business/term financing loan so that he/she has the finances required to start the new shop.

How Much Interest Does The SME Have To Pay?

The amount of interest that the SME has to pay on a business financing loan is subjective. There isn’t a definitive guide on the interest rate payable. In most cases, the P2P platform will do its own assessment of how risky it is to lend money to the SME. Once the interest is determined through a credit underwriting process, the loan request will then be put up on the P2P platform to crowdfund money from investors.

Many small businesses are also exploring non traditional funding sources for SME loans.

3. Property-Backed Financing

For SMEs with the luxury of owning a property, you can also raise capital using your property as a collateral. This is similar to invoice financing where you use the invoice as a collateral. In this case, the property becomes a collateral.

Compared to invoice financing, property-backed financing is much safer. As such, the interest rate that P2P investors can earn from is also lower.

2. Bridging Loan

Another type of short-term financing that works in a similar way to P2P loan is bridging loan. Because of the similarity between P2P loan (property-backed financing) and bridging loan, you might be tempted to classify the two of them as the same thing. However, they are not, and they have a number of dissimilarities. Before we go into the details of their dissimilarities, let us first define what is a bridging loan. You can also have a bridging loan when you apply for a home loan for a new house whilst still processing the selling of your current house.

What Is Bridging Loan?

Bridging loan is also a short-term financing option. However, the main purpose of bridging loan is to ‘cover’ (or bridge) the gap between an incoming debt and the time till your credit is ready.

How Does Bridging Loan Work?

The best way to explain how a bridging loan works is by giving an example. So, imagine if you just sold your house. It will take a while before you receive proceeds from the sale, isn’t it? But what happens if you need the money to pay for your down payment to purchase your new home? This is where bridging loan can come in and help to pay for your new home while you wait for sales proceeds from your existing property.

What Is The Duration Of Bridging Loan?

Since bridging loan is a type of short-term financing, the bank/financial institution will generally offer you 6-12 months of loan period. You will need to fully repay the loan after the 6-12 months period.

2 Types Of Bridging Loan: Capitalised Interest Bridging Loan & Simultaneous Repayment Bridging Loan

Capitalised Interest Bridging Loan

Under the capitalised interest bridging loan, the bank/financial institution will finance your new home (up to 80%). Once the sale of your current property is completed, the repayment of the bridging loan will start. Interest will be accrued and payable to the bank/financial institution for the whole period of your bridging loan.

Simultaneous Repayment Bridging Loan

But even if you haven’t sold your property yet, you can still take a bridging loan. This is the purpose of the simultaneous repayment bridging loan. The simultaneous repayment bridging loan is for homeowners who have the intention to sell off your current property. But you might not have found a suitable buyer yet. In such cases, you can take the simultaneous repayment bridging loan to pay for your new home while continuing to pay off the home loan for your current property. The bank/financial institution will likely give you up to 12 months to sell off your property. After which, you will need to repay your bridging loan once you receive the sales proceeds.

What Do You Need To Qualify For A Bridging Loan?

In order to qualify for a bridging loan, you will need to show proof that you are waiting for sales proceeds from your previous property. This can work by providing the Option to Purchase (OTP) agreement document that is signed by the buyer.

Is Bridging Loan Only Limited To Private Property Owners?

Bridging loans do not have a specific target audience. Regardless of whether you are a private property or HDB owner, you will be able to apply for a bridging loan as long as you have the OTP agreement for your current property. It also doesn’t matter whether the property you are selling away is an HDB or private property.

Where Can You Get A Bridging Loan?

Bridging loans are offered by most financial institutions and banks in Singapore. Typically, if the bank or financial institution offers home loan, it will also offer bridging loan to you.

3. P2P Loan vs Bridging Loan: 3 Distinct Ways That They Are Different

1. The Target Audience Is Different

P2P loan is a category of loan that is mainly targeted at SMEs which need short-term financing whereas bridging loan is specifically targeted at homeowners. In particular, bridging loan is targeting at existing homeowners who are looking to sell your current property and switch to another property.

2. The Provider Of The Loan Is Different

The financing of P2P loan comes from accredited investors. Under Singapore’s law, an accredited investor means that you need to own personal assets of at least $2M, have an income of at least $300k in the last 12 months or own a company with at least $10M in net assets. If you are an accredited investor, you will be able to borrow money to SMEs who are looking for financing on P2P lending platforms.

The financing of bridging loan comes from either banks or financial institutions. No other types of companies or individuals can offer bridging loans.

3. The Interest Rate Payable On The Loan Is Different

For bridging loan, the interest rate payable is pretty stable across the industry. Banks and financial institutions are likely to offer very similar interest rates to each other. Unlike bridging loan, P2P loan doesn’t have a stable set of interest rate for each of them. Every P2P loan request is different and unique to itself. Even the same P2P loan request can end up having different interest rate on different P2P lending platform.

Want to learn how bridging loan can help you in your bid to become a multi-property owner? Get in touch with iCompareLoan where our loan specialists will show you how to leverage on bridging loan in your second property purchase.

Connect with Paul Ho (Founder of iCompareLoan) on linkedin.