Singapore Property Investment Sales Market Likely to Rebound on Renewed Optimism says CBRE’s New Research

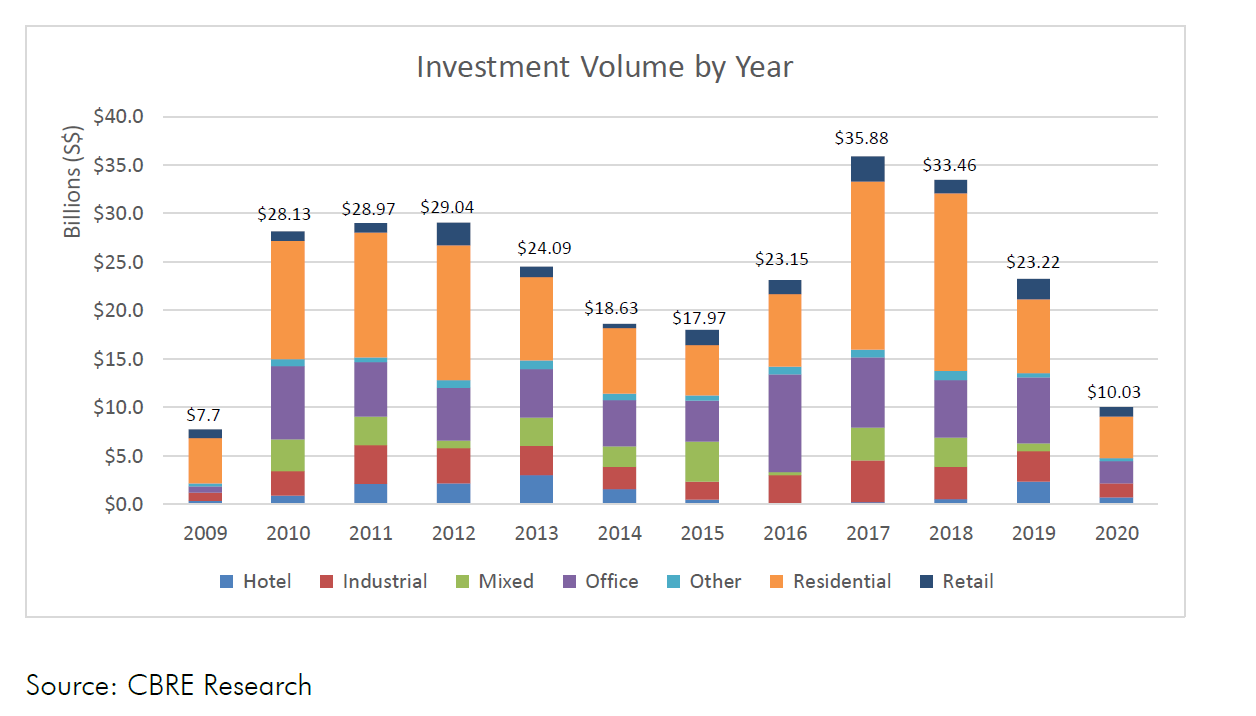

According to CBRE Research, preliminary real estate investment sales volume in Singapore in 2020 year-to-date came to S$10.03 billion. This reflected a 56.8% drop from the previous year, marking the lowest investment sales volume since the financial crisis in 2009 (S$7.7 billion). On a quarter-on-quarter basis, Q4 2020 volume eased by 23.9% to S$2.14 billion.

Mr Desmond Sim, Head of Research, Singapore and Southeast Asia at CBRE, says, “As a result of the pandemic, it was unsurprising that investors preferred to sit by the sidelines as they wait for value to emerge. This year, the low volume was also attributed to zero sizeable deals, which we define as transactions of more than S$1 billion. Due to the widening gap between buyer-seller expectations, some deals were unable to materialize. In fact, 68.9% of the total deals in 2020 year-to-date were bite-sized transactions of less than S$25 million.”

Additionally, given the global travel restrictions, foreign capital inflows have almost halved from the previous year, dropping by 53.0% y-o-y to S$3.18 billion in 2020. This was more pronounced in the second quarter of the year when market activity was hindered by government-imposed restrictions.

Property investment sales market in 2020 were propped up by the luxury residential market and government land sales.

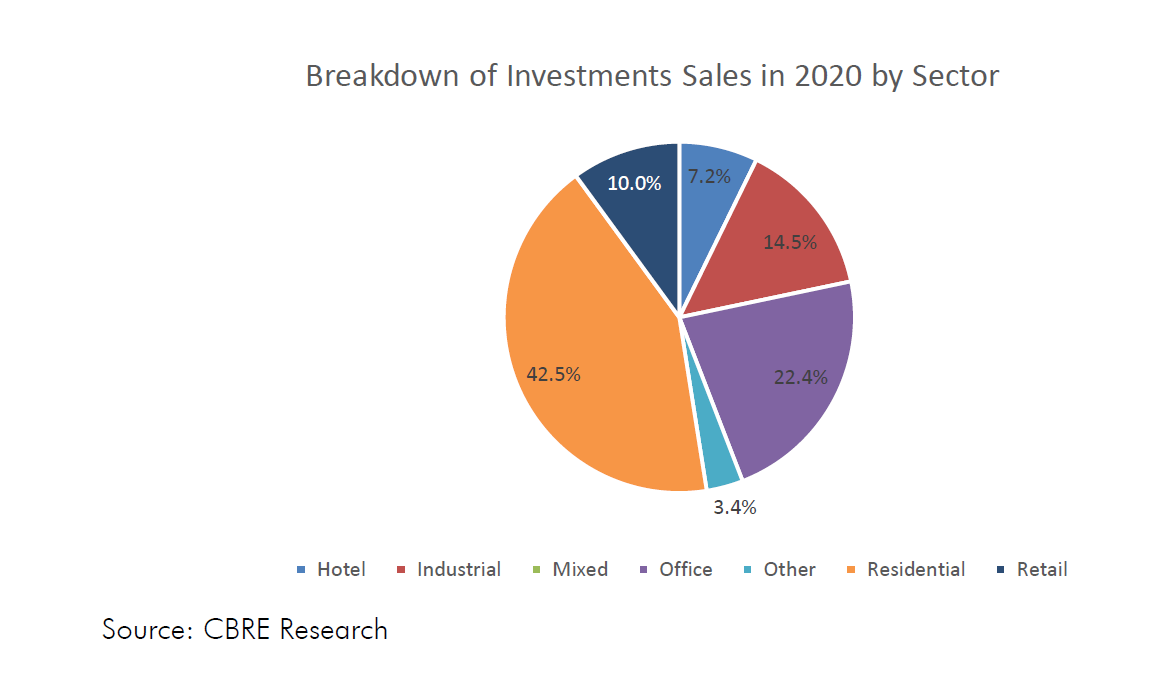

Of the total property investment sales volume of S$10.03 billion in 2020, residential sales made up 42.5% (S$4.26 billion). And of this S$4.26 billion of residential sales, S$1.52 billion is contributed by government land sales for residential use.

Encouraged by the strong sales in project launches, as well as the declining inventory of unsold units, developers have turned to government land sales and even the private market to acquire land. This is evident from the strong bidding activity on the most recent tender close (Yishun Ave 9 and Tanah Merah Kechil sites), as well as the spate of en-bloc activity in Districts 14 and 15, where residential sites along Guillemard Road, Haig Road and Katong Road were sold.

The office and industrial sectors also came in strongly, contributing 22.4% and 14.5% of property investment sales market, respectively. Despite telecommuting trends, prime office assets in Singapore remain attractive to investors for their stability and yield. This appeal is further strengthened by the redevelopment potential of core office assets under the Central Business District Incentive scheme, where properties are eligible for a bonus plot ratio of 25-30% if redeveloped into mixed use. Meanwhile, industrial assets saw a surge in demand this year due to stockpiling and e-commerce.

Looking into 2021: Rebound expected on renewed optimism

Mr Michael Tay, Head of Capital Markets, Singapore, at CBRE, says, “The Singapore investment market has always been resilient, and it has demonstrated in past cycles of its ability to recover from crisis situations. This was apparent post Global Financial Crisis when real estate investment sales volume improved by a strong 265.4% in 2010.”

Property investment sales market in Singapore are likely to get a shot in the arm as vaccination programs are rolled out, with business sentiments picking up and border restrictions gradually eased.

Mr Tay continues, “Investors are likely to remain discerning at the beginning of next year. Nonetheless, spurred by the low interest rate environment and ample liquidity, investors will still be constantly in search of investments that provide them with higher returns, coupled with stability and value at the top of their minds. As an investment destination, Singapore fits this bill perfectly given its proven ability to handle the pandemic, macroeconomic stability and political-neutral stance.”

Consequently, CBRE opines that property investment sales volume in 2021 is likely to rebound, led by residential, office, and industrial sales. There will also be renewed interest in retail and hospitality assets, as investors are on the prowl to buying these assets on the cheap.

In an earlier report CBRE said that office rents are expected to improve in the second half of 2021, resulting in an overall positive rental growth for the whole of 2021.

This is on the back of Ministry of Trade and Industry’s projection that the Singapore economy will grow by 4% to 6% in 2021. Nonetheless, office demand is expected to remain relatively subdued in 1H 2021, as firms will still remain cautious in the wake of the COVID-19 pandemic. Should economic activity and business sentiment recover after the administration of the vaccine by Q3 2021, the office market is well poised to benefit from the gains in employment.

Five new projects are estimated to complete in 2021, which will add another 1.23 million square feet to the entire office stock. Out of these five, there is only one Grade A office development – CapitaSpring, which will add another 0.65 million square feet of office stock to the Grade A (Core CBD) market.

Mr Desmond Sim, Head of Research, Singapore and Southeast Asia, CBRE, says, “Leasing activity is improving, as we understand that there are currently more ongoing negotiations for CapitaSpring which is slated to complete next year. The initial office supply pressure for 2022 has been dissipated due to construction delays, but which augured well for the office market as it provided more time for pre-leasing activities. The future supply that will spread over a longer time horizon allows demand and supply dynamics to recalibrate.”

Although there is a limited supply of new Grade A developments in the pipeline, CBRE Research expects that Grade A (Core CBD) occupancy will face further downward pressure in the early stages of 2021.