List Sotheby’s International Realty (List SIR) noted in its recent research that it will take 2 – 3 years to see how the residential property market pan out here.

The research noted that it was just slightly over a year ago that the government introduced a new set of cooling measures to “cool the property market and keep price increases in line with economic fundamentals”. The reasons cited were that homes prices were running ahead of economic fundamentals, a large supply of units was coming onstream and interest rates were going up.

“As of July 2019, the fear of interest rates rising has become benign when the US Federal Reserve lowered its benchmark rate by a quarter point, with hints of one more cut before the end of the year. As for home prices, the price index moderated by a total of 0.7% over two quarters in Q4 2018 and Q1 2019 but resumed its upward trend in Q2 2019 when it rose by 1.5% from the previous quarter. This rise could be attributed to the strong take-up seen in some new projects which are priced higher than existing projects in the neighbourhood. These include Amber Park, Boulevard 88 and Sky Everton.

Just how big is the supply that was generated by the collective sales frenzy which lasted for about two years from mid-2016 to mid-2018, driving up land prices at the same time?

How the residential property market pan out till date?

According to List SIR, there were some 90 private land sale sites sold in the period which could potentially yield 25,000 new homes. Combined with the supply of around 14,000 units from the sites sold under the government land sales program, a total of 39,000 new homes were expected to be supplied to the market. In addition, there were 5,000 units from sites that are pending approval as at end-June 2019. This brings the total supply in the pipeline to around 44,000 units.

“To put things into perspective, following the last collective sale frenzy in 2006-2007, there were 43,400 unsold units as at Q2 2008, a number similar to the current situation. About half of this number was contributed by the collective sale sites. At that time, the global economy was hit by the Global Financial Crisis in the US and Europe which lasted for about seven years. The recovery in Asia was unexpectedly fast as it benefited from the massive fiscal and monetary stimulus introduced by the United States and European economies. Successive cuts in interest rates and the inflow of foreign funds into the Singapore residential market helped to absorb an average of 15,500 new homes in the three years from 2009 to 2011.”

List SIR said that the present circumstances are quite different, in that the escalation of the US-China trade conflict coupled with the weaker growth of the Eurozone economy has led to a global economic slowdown.

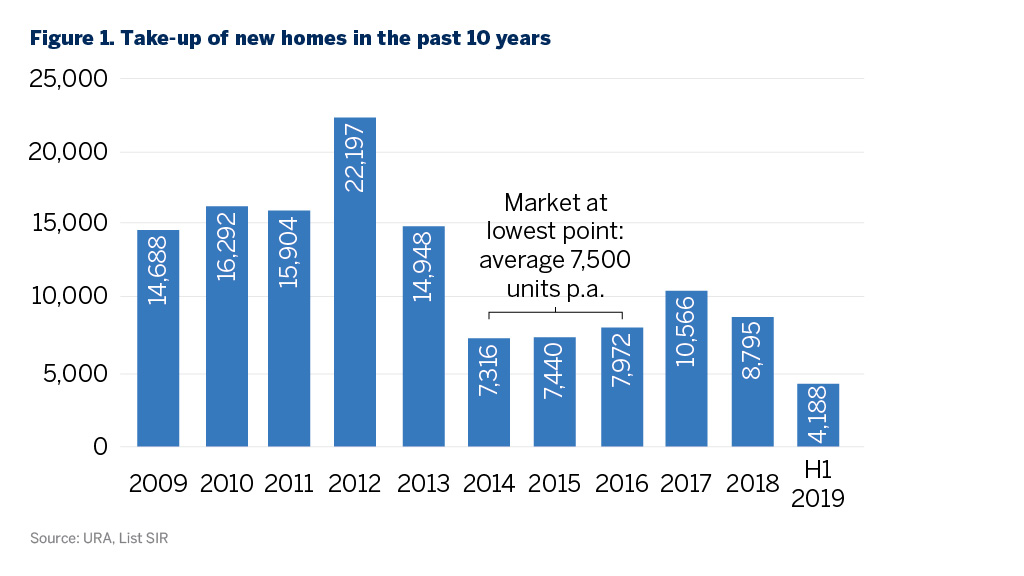

“Demand for new homes in 2018 had slowed to 8,800 units from the 10,566 units in 2017 (Figure 1). In H1 2019, some 4,200 new homes were sold. With the economy expected to slow down further in H2 2019, the take-up rate is likely to be at a similar level. This will bring the whole year’s new home sales to around 8,500 units, slightly higher than the fundamental demand of 7,500 units.”

State of the current market and how will the residential property market pan out

Table of Contents

In assessing the current status of the 39,000 new homes generated from the active land-banking activity of developers in 2016 to 2018, List SIR said that the collective sales market ground to a halt after cooling measures were announced in July 2018 as developers now have to pay a non-remittable additional buyer’s stamp duty (ABSD) at 5% upon purchase of development sites plus 25% ABSD upon the failure to sell all units in five years. It noted that in order not to aggravate the strong supply pipeline further, the government also reduced new supply from its land sales programme in 2019. This would allow some buffer time for developers to clear the supply pipeline.

“Up to end-August 2019, developers have supplied around 23,000 new homes for sale (Figure 2 and 3). Of this number, around 10,800 units (47%) have been sold.The remaining 12,200 units (53%) are still unsold. The bulk of the unsold units are found in the Rest of Central Region (RCR) and Outside Central Region (OCR) mainly because the project sizes are bigger compared to those in the Core Central Region (CCR). While 78% of the units in CCR were unsold, the 1,306 units is less than a quarter of those in either RCR or OCR.

For the 5,666 unsold units in RCR, slightly over 1,000 units are found at the Outram/Havelock area, followed by around 800 units each in the Potong Pasir/ Serangoon Road area and Amber/ Meyer Road area.

As for the 5,240 unsold units in the OCR, nearly 2,600 units are located in the Hougang/ Upper Serangoon Road area while another 1,900 units are located in the Tampines/Upper Changi Road area.”

List SIR said that the supply pipeline that was not yet launched for sale as at end-August was nearly 16,000 units. Similarly, 74% of these units are in projects located in RCR and OCR where the larger projects are found. Of the 6,002 units in OCR, some 1,300 units are located in Hougang/ Sengkang area and another 1,100 units are located in Upper Bukit Timah area. The remaining 3,600 units are scattered in various suburban locations.

For the 5,776 units in the RCR, around 1,400 units are located in the Outram/Bukit Merah area. Another 1,000 units are located in the Toh Tuck Road neighbourhood while the rest are located in several city-fringe locations, including the mega 1,862-unit project at Normanton Park.

In the CCR, about 1,700 units of the supply pipeline of the 4,178 units are located in the Holland Road area while 1,000 units can be found in the Orchard Road/Cairnhill/ River Valley Road area. The Bukit Timah enclave holds some 800 units of this supply.

How soon can the market absorb the supply pipeline and how will the residential property market pan out?

List SIR said that with 12,200 unsold units from the projects already launched by August 2019 and including the 16,000 units from future projects, it is looking at a total of 28,200 units to be absorbed by the market.

“Assuming an annual take-up rate of 8,500 units, it will take about 3.5 years to clear this unsold stock. This will take up to the end of 2022. What it means is that developers of projects which are built on sites that were purchased in 2017 or earlier and are not fully sold by then, will be liable for the 15% ABSD plus interest at 5% p.a. However, should demand improve to say around 10,000 units per year – if the brisk sales seen at One Pearl Bank and Parc Clematis are replicated by upcoming launches – then it will take less than three years for developers to clear the entire supply pipeline. :

List SIR said that it was cognizant of the challenging external circumstances that has impacted the Singapore economy, market sentiments have dampened.

“Developers have to continue to work at right-sizing and right-pricing to bring potential homebuyers to the point of commitment. As Singapore’s population growth is now less than 1%, the city state has to depend on foreign funds to invest in our real estate, especially at the higher end of the market. The next two to three years are critical to see how will the residential property market pan out.”

How to Secure a Home Loan Quickly

Are you planning to invest in private properties but ensure of funds availability for purchase? Don’t worry because iCompareLoan mortgage broker can set you up on a path that can get you a home loan in a quick and seamless manner. We are the experts who do the work for you for free, while you lean back, rest and rely on our professionalism at absolutely no cost to you.

Our brokers have close links with the best lenders in town and can help you compare Singapore home loans and settle for a package that best suits your home purchase needs. Find out money saving tips here.

Whether you are looking for a new home loan or to refinance, the Mortgage broker can help you get everything right from calculating mortgage repayment, comparing interest rates all through to securing the best home loans in Singapore. And the good thing is that all our services are free of charge. So it’s all worth it to secure a loan through us.

For advice on a new home loan.

For refinancing advice.