Singapore residential market is projected to exhibit both volumes and price weakness in 2019, said a recent research paper by DBS Research Group.

The report in saying that the Singapore residential market is waiting for its turn to shine said that while there is good value in developers’ share prices, judging by historical trends in past property down-cycles, developers are likely to trade in a lower range until macro conditions turn up.

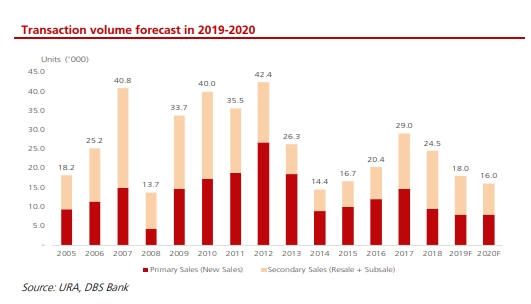

In noting that the Singapore residential market have peaked, while prices and volumes are on a downtrend in 2019., the research report said that given the surprise introduction of property cooling measures and uncertainty arising from new “minimum size” rules in 2018, the bank projects buyers to hold off purchases.

It further expects primary sales transaction volumes to fall 20 per cent year-on-year to 7,500-8,500 units while. It also predicted the the property price index (PPI) to fall even further if the macro conditions worsen.

With close to 40,000 units in the Singapore residential market ready for launch in a slowing market, the odds of achieving strong sales during launches are against developers, it noted.

With close to 40,000 units in the Singapore residential market ready for launch in a slowing market, the odds of achieving strong sales during launches are against developers, it noted.

The report said that displaced en-bloc buyers are unlikely to be the “boost” that developers are hoping for in 2019; and that Singapore residential market expectations of a boost in sales volumes from displaced en-bloc households up to middle of 2018 might not materialise.

The report said that assuming that these home owners are paid nine months after the close of the en-bloc tenders, it estimates that only 11 per cent of the total 8,500 en-bloc households will receive their monies in the 1st Half of 2019.

“Therefore, we believe that most of the buying from these displaced households will already be done before that and will not be a significant boost to sales volumes in 2019…

“New cooling measures to raise uncertainty in the property market. We believe that the recent introduction of cooling measures in July and October 2018 will create uncertainty and curb investors’ interest in the property market in the immediate term.

“The revised additional buyer stamp duty (ABSD) and loan-to-value curbs imposed in early July 2018 have effectively raised the cost of acquiring a new home which we believe will impact investors and foreigners the most, while keeping the genuine homebuyers or home-upgraders largely spared.

“Based on an assumed S$1.5m price for a new home, we estimate that the new measures will raise the transaction costs by an additional S$75,000 for home buyers (from higher cash down payments from tighter loan limits). For investors and foreigners, the cash and/or CPF commitment increases by a hefty S$150,000 (S$75,000 each from higher ABSD payable and upfront capital).

“The policy announced in October 2018 regarding the reduction of average minimum size for developments which will be effective for new developments approved from early January 2019 infused more uncertainty in the market. This will be a dampener on sales volumes as we believe that homebuyers and potential investors who are not in a hurry might adopt a “wait-and-see” attitude before committing to a purchase of a new home.

“Primary sales demand to drop back to 7,500-8,500 units in 2019. The slowdown in sales momentum has already happened, as evident in the primary sales momentum falling to c.500-800 units per month since July 2018…which we believe will remain the “new normal” going into 2019.

“As such, we project primary home transaction volumes to fall to 10,000-11,000 units in 2018 (YTD 11M18 transaction volumes reached c.9,300 units sold). Thereafter, we expect primary market volumes to decline to 7,500-8,500 units per annum, in line with home formation levels. This is similar to the transaction volumes seen back in 2014-2016, post the last round of cooling measures introduced from 2010-2013.

“En-bloc buyers to still boost the market in the near term but impact to taper off from 2H19. With an expectation of a slowdown in transaction volumes in 2019, we see near-term sales being boosted somewhat as home owners look for a replacement home from 2019 after receiving their proceeds from the en-bloc. Based on our estimates, assuming that these home owners are paid nine months after the close of the enbloc tenders, we estimate another c.S$4bn could be paid in 1H19 or close to another 1,000 units.

“While demand for replacement units may be strong near term, we question the

longer-term sustainability of demand from en-bloc buyers.”

The report noted that Singaporean households remain the key buyer of new homes, and that based on data compiled by Realis as at 27 November 2018, out of the 22,000 units transacted in the first 11 months of 2018, a majority of the buyers in 2018 were Singaporean households, accounting for close to 79% of total sales with Singapore permanent residents (PRs) accounting for another 15% and the remaining 6% from foreigners.

Foreigners and PRs who are active in the property market come mainly from China (6.1% of total PR and foreigner transactions), followed by Malaysia (3.8%), India (1.8%) and Indonesia (1.8%). The report said that close to 34 per cent of sales are made to upgraders looking to purchase a private home.

The research report said that while the Singapore residential market is expected to remain weak, the commercial real estate prospects remain bright given positive demand-supply dynamics.

How to Secure a Home Loan Quickly

Are you planning to invest in properties but ensure of funds availability for purchase? Don’t worry because iCompareLoan mortgage broker can set you up on a path that can get you a home loan in a quick and seamless manner.

Our brokers have close links with the best lenders in town and can help you compare Singapore home loans and settle for a package that best suits your home purchase needs. Find out money saving tips here.

Whether you are looking for a new home loan or to refinance, the Mortgage broker can help you get everything right from calculating mortgage repayment, comparing interest rates all through to securing the best home loans in Singapore. And the good thing is that all our services are free of charge. So it’s all worth it to secure a loan through us.

For advice on a new home loan.

For refinancing advice.