The impact of trade tensions may be starting to affect Singapore SMEs that are most exposed to global trade, a study of the payment data of more than 120,000 companies in Singapore across a broad range of sectors has indicated.

DP Information Group (DP Info) which released the findings of the study on Nov 8 said the payment patterns of Singapore SMEs across eight major sectors were analysed in terms of timeliness – payment within terms, within 90 days and above 90 days.

DP Info is Singapore’s leading provider of information, analysis and intelligence on the Singapore corporate sector. Part of Experian, the world’s leading global information services company, DP Info offers a range of powerful tools for assessing the credit worthiness and financial health of both companies and individuals.

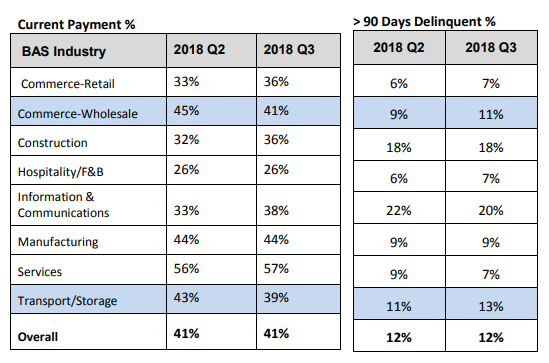

The proportion of Singapore SMEs in the commerce-wholesale sector that made their payments within terms declined from 45% to 41% quarter on quarter (QoQ), for the period ending September 2018.

Table of Contents

For the transport/storage sector, it decreased from 43% to 39% for the same period. These two sectors also registered a marginal increase in the proportion of SMEs that are more than 90 days delinquent. The proportion of SMEs in the commerce-wholesale sector which were more than 90 days delinquent went up from 9% to 11% QoQ. For the transport/storage sector, it increased from 11% to 13%.

https://www.icompareloan.com/resources/sme-financing/

However, in general, delinquency rates across the Singapore SME sector were stable.

Mr James Gothard, General Manager, Credit Services & Strategy SEA of Experian, said: “Over the past year, there has been an increase in US-China trade tensions, associated with tariffs, which may be beginning to show its effect. Commerce-wholesale and transport/storage are the sectors that can be impacted by global trade tensions.”

Mr Gothard added: “Trade tariffs, through their downstream effects, have the potential to impact Singapore’s SMEs in a number of ways – by reducing the competitiveness of their exports and by affecting sales in overseas markets. Even if a specific country is not the target of tariffs, demand for intermediate goods from a country that is the target can be impacted.”

In the last quarter ending September 2018, business sentiment among SMEs for the six months to end-March 2019 have also dampened, with lower revenue and profitability expectations across all sectors, as indicated by the SBF-DP SME index.

In the backdrop of the US-China trade tensions, Singapore SMEs in general have become more cautious, but this has been tempered by regional opportunities in Southeast Asia as well as by the year-end festive season which is likely to be marked by an uptick in spending.

Mr Gothard said: “A considerable number of Singapore SMEs still derive their revenue sources from external markets. Coupled with increasing domestic competition, there may well be a reprioritisation of market opportunities, with greater focus on emerging marks such as the Philippines, India and Myanmar.”

Mr Paul Ho, chief mortgage officer of iCompareLoan, said The challenges of Singapore SMEs remain serious and bears the brunt of the bad economy.

Mr Ho said, “Singapore SMEs deliver less GDP than big companies but hire a disproportionately high percentage of a country’s work force. Without SMEs, unemployment could go up so much higher. SME loans are important for SMEs who are always short of cash. It would be prudent for SME bosses to read more about the different types of financing in Singapore.”

He added: “Many established SMEs are family businesses that have been around for 10 to 20 years, many have suffered cyclical downturns and could be wound up if they do not have cheap funding. This is the time when these businesses need to stay trim, access cheaper source of funding and cut cost. If the downturn is long term, then such businesses should not access working capital loans for businesses that may have entered into negative gross margins as they will end up owing even more debt.”

https://www.icompareloan.com/resources/sme-loans/

Singapore SMEs should remember that they need to borrow when they do not need money. If they try to borrow when their business is struggling and they need additional funding to tide over a tough patch, then they will find that their access to funding is completely cut off and they may end up with very expensive funding.

Mr Ho said: “It may be wise to plan 6 to 12 months ahead for any potential funding needs. Even if you do not need funding now, you may want to quickly refinance your home loans for any potential equity and stand-by cash even if you do not need it now.”

He added: “Remember, banks assess your credit and affordability at the point of application, so you should apply when your status is good, not when you have further deteriorated. At that time, no banks will lend you.”

You can read more about the different types of funding here. If your business is profitable and you only need short term funding, but your access to bank’s working capital is temporarily cut off, then you should consider personal loans as a source.

by: Hitesh Khan / Contributor iCompareLoan

How to Secure SME Loans Quickly

If you are searching for SME loans, the loan consultants at iCompareLoan can set you up on a path that can get you a it in a quick and seamless manner. Our loan consultants have close links with the best lenders in town and can help you compare various loans and settle for a package that best suits your needs. Find out money saving tips here.

Our Affordability Tools help you make better property buying decisions. iCompareLoan Calculators help you ascertain the fair value of a property and find properties below market value in Singapore.

To find out more about Peer to peer lending versus that of SME loans so as to make an informed decision: SME Loans or Peer-to-peer (P2P) Lending – What is the difference?

Contact us for advice on a new SME loans.

Contact us for home loan or refinancing advice.