TDSR Causes Home Loan Refinancing Hardships

By PAUL HO

In this article, we will look at how Total Debt Servicing Ratio (TDSR) affects refinancing. According to MAS, if you were to refinance to another bank or simply to reprice with the same bank, you will still be required to pass Total Debt Servicing Ratio (TDSR) of not more than 60%.

Why would people refinancing be hurt?

Table of Contents

So who are the people who might be hurt? Many people who had bought their properties using 35 years loan tenure or under a less stringent Debt Servicing ratio of 60%. Note: Debt Servicing ratio of 60% is not the same as Total Debt Servicing Ratio of 60%.

Many people who have borrowed under interest-only financing would also be hurt with increase in interest rates as they cannot switch.

If they do switch, they will incur higher monthly servicing cost, and therefore fail the TDSR threshold of ≤60%.

Case of interest-only borrowing

Many of these financial institutions provide a “Step-up” home loan package, so these property owners are now stuck with increased financing costs and yet cannot refinance their home loan due to failing the new TDSR rule.

All refinancing will have to pass the TDSR rule.

Case of 30-year loan refinancing

This individual got approved under a Debt servicing ratio (DSR) of 60% based on a lower interest rate set at 2%. The monthly installment works out to be $3,252 per month. This means that based on DSR, this person is only at 36.14%. This calculation does not consider his car loan.

Figure 1: DSR of 60% using 2% interest rate to justify (Source: www.iCompareLoan.com)

He earns $9,000 a month and pays $3,255.65 monthly for his mortgage, this is quite affordable. Even if the bank takes into consideration his car loan of $1,500 a month for the computation of the Total Debt Servicing Ratio, he would still PASS at 55.70%.

But with the new rule, the TDSR must be assessed using a prescribed rate. According to MAS, the financial institution must “apply a specified medium-term interest rate or the prevailing market interest rate, whichever is higher, to the property loan that the borrower is applying for when calculating the TDSR”.

This medium-term rate is 3.5% for housing loans and 4.5% for non-residential property loans.

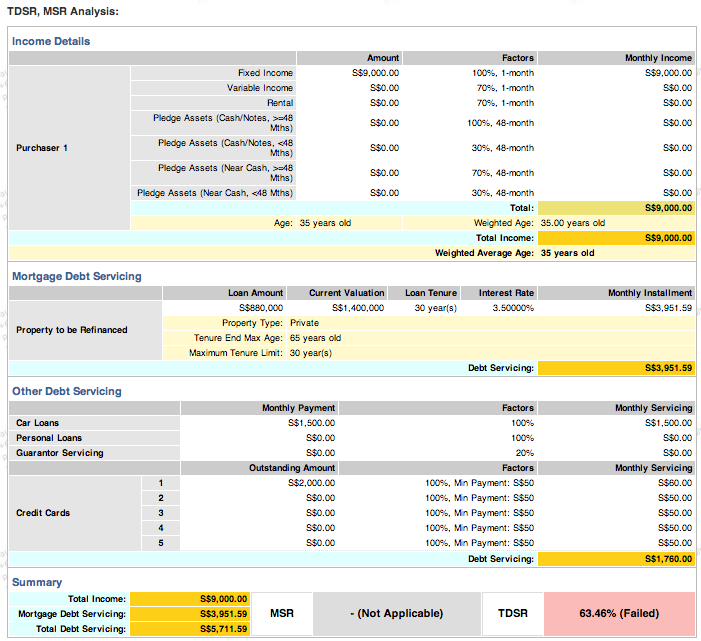

Figure 2: TDSR at 3.5% – www.iCompareloan.com Home Loan Report (TM)

So in this case, if we use 3.5% as the assessment interest rate, amounting to $3951.59, then this Mr. Tan Ah Kow, will fail TDSR at 63.46%. This means that Mr Tan cannot refinance with the current bank to reap interest savings. If, at this point, the bank starts to raise the interest rate on his current loan, he is compelled to pay the higher rate as he is not eligible to refinance.

IN SUMMARY

While the MAS means well to put in place regulation to ensure financial prudence amongst financial institutions, this new rule actually traps a group of property owners who now cannot refinance to cheaper rates and are trapped by the banks who first offered them these highly leveraged lending. And we’re not even talking about extreme cases. In all measure, Mr. Tan Ah Kow earns a decent salary at $9,000 a month and is considered a high income earner.

So the purpose to rein in aggressive lending from banks actually benefits the banks who initially took the risks to lend more aggressively as they now have a group of home owners who cannot refinance and are trapped in higher rates through the higher spread charged by the bank.

Isn’t it ironic that the regulation ended up hurting those people who took the loan rather than impose financial prudence on the aggressive financial institutions?

This is like telling the bad boy to behave so that you will give him a sweet. But the bad boy knows that he will be given a sweet if he is bad, he may test the system again to be given get another sweet. This is negative reinforcement.

Do check out the consultants at iCompareLoan who can help you to Compare Singapore Home Loans and assess whether you will be able to refinance to save on interest costs.

For advice on a new home loan.

For refinancing advice.

Download this article here.