How Do I Compare Home Loans in Singapore?

By PEARL LIM

Taking a mortgage to finance a residential property is a heavy financial liability for most; thus it is a decision that shan’t be taken lightly. This article provides a starting point and some basic things to consider before shopping for a mortgage.

Loan types

Table of Contents

You can select from an array of loan packages available in the market. These can be broadly classified as

- Fixed rate loan

- Variable (floating rate) loan

- Combo (hybrid) loan

- Cashback or cash-incentive loan

- Interest-offset loan

- Interest-only loan [Do note that interest-only mortgages for residential properties have been disallowed by MAS (Monetary Authority of Singapore – Singapore’s central bank) since14 Sep 2009, MAS Notice 632]

To read about the exact definition of each of these, go here.

The most popular types are the fixed-rate package and variable (floating rate) package. For the former, the interest rate are only fixed for a period of 2-5 years, after which rates are allowed to float. The latter, however, has rates that fluctuate throughout the loan duration. The interest rates for fixed rate are usually higher than for variable, in order to compensate the bank for keeping rates stable. To understand more about the nuances between the two and which to select, do look at our previous article: “Fixed-Rate Versus Floating Rate Home Loan Packages in Singapore: Which is Right for You?”.

Further, for each of the 6 types listed above, you may find different variants. For example, for the Variable (floating rate) loan, the interest rate can be SIBOR-pegged, SOR-pegged or an average of SIBOR or SOR. Others may also offer a cap on the upper limit of the interest. For a detailed discussion about choosing between a SIBOR or SOR based loan, read “Understanding SIBOR and SOR Based Home Loans in Singapore”.

If you feel flushed by the myriad of loan types and muddled by which to choose, you should consult a mortgage consultant.

Interest cost

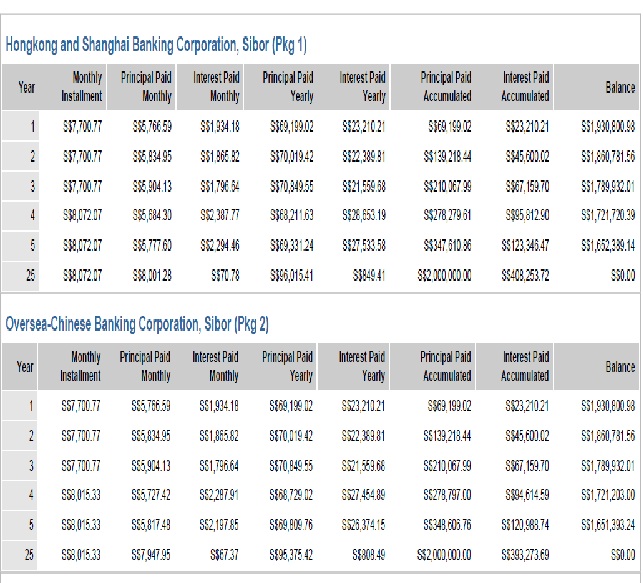

Interest is the cost of borrowing. So naturally it is a key deciding factor when selecting a loan. You will not want to pay an excessive price for borrowing; therefore take note of the interest rate over the entire life of the loan, not just in the beginning. To compare the interest payable for different loans, you can make use of the loan analysis system at iCompareLoan.com, which can generate reports showing the interest incurred for all the mortgage packages in Singapore. Figure 1 and 2 show a snapshot of the interest comparison tables and charts to be found in our reports.

Figure 1

Figure 2

Conditions of the package

- Lock-in period (or commitment period)

- Clawback period (or reimbursement period)

- Conversion (or repricing if there is no cost involved)

Interest costs aside, you should look out for other features in the package that can add to the cost of the loan; particularly, when you intend to make partial or full repayment, refinance or sell the property in a few years’ time.

Any repayment during the lock-in period (normally the first 2 to 5 years of the loan) will result in a penalty of usually at most 1.5% of the redeemed amount. But some packages do not come with a lock-in period. You can consider these if you foresee early repayment.

The clawback period, on the other hand, is the period (typically the first 3 years) in which a full redemption of the loan will incur a refund of all the freebies given such as legal subsidies, valuations, etc. The cost of these perks usually total $2,000 to $3,000.

Do note that MAS passed a ruling stating that cash rebates (including legal subsidy and stamp duties) offered in a mortgage have to be deducted from the purchase price, which effectively lowers the loan quantum. This has caused many banks to stop offering subsidies of any sort since mid-2012. However for those that still do, there may remain a claw-back period.

Finally, some loan packages have a free one-time conversion (repricing) to another loan package with a different interest rate or structure. So before you refinance, you should ask your current financier if they offer free repricing. Repricing can less costly then switching to another financier.

For advice on a new home loan.

For refinancing advice.

Download this article here.