DBS Research referring to latest MAS statistics said that industry loan growth momentum maintained amidst volatile macroeconomic conditions.

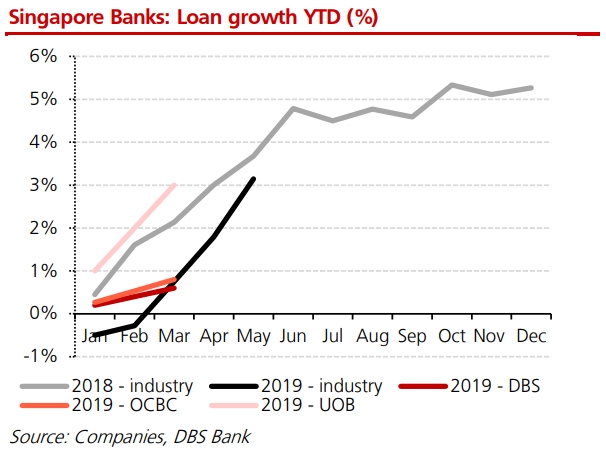

- Industry loan growth momentum maintained; YTD loan growth at 3.1%

- Business loans growth continues to lead consumer loans

- Mortgages loan book declined for fourth consecutive month

- Deposit growth outpaced loan growth; cost of deposits unlikely to come down

DBS Research said on June 28 that according to the statistics released by the Monetary Authority of Singapore (MAS), industry loan growth (DBU + ACU1) for May 2019 grew 4.7% y-o-y and 1.3% m-o-m (Apr 2019: +4.0% y-o-y/ +1.0% m-o-m), as business loans growth (+1.6% m-o-m) offset sluggish consumer loans growth (+0.5% m-o-m). Year-to-date, loans grew 3.1%, in line with our full year expectations of c.5% growth.

The Research added that manufacturing, building and construction, and transportation loans continued grow strongly by 16.6%,15.2% and 9.1% y-o-y respectively, against shrinking general commerce and financial institutions loans of 1.5% and 2.4% y-o-y. Meanwhile, consumer loans growth is still slowing, by c.1.2% y-o-y due to a slight 0.3% y-o-y contraction in mortgages. At its peak, mortgage loans grew 4.7% y-o-y in May 2018.

“For the fourth consecutive month, Singapore’s mortgages book declined m-o-m, registering 0.1% m-o-m drop in May 2019. We continue to track the sales progress of new residential development projects, seeing more new launches in May-Jun 2019. We do not expect the mortgage book to see a deep contraction unless there is an accelerated slowdown in the economy with massive unemployment.

Overall deposits recorded strong growth of 7.4% y-o-y, outpacing loan growth, led by fixed deposits as depositors sought higher fixed deposit rates currently on offer. Our channel checks across various banks indicate that SGD fixed deposits are still in demand by both local and foreign banks with competitive interest rates offered and decent interest from recent issues of Singapore Savings Bonds.”

On July 22, it said that Singapore Banks’ earnings likely to be supported in 2Q. DBS Research said that Singapore banks are expected to continue to be on track for decent 2Q19 drawdowns and are also likely to meet full year loan growth guidance.

On July 22, it said that Singapore Banks’ earnings likely to be supported in 2Q. DBS Research said that Singapore banks are expected to continue to be on track for decent 2Q19 drawdowns and are also likely to meet full year loan growth guidance.

DBS Research’s preferred pick is UOB.

“Singapore banks are due to declare interim dividends alongside 2Q19 results (DBS: 29 Jul 2019, OCBC and UOB: 2 Aug 2019). We believe that with the existing macroeconomic conditions alongside some market uncertainty, there is unlikely to be any upside surprises on dividends as banks would prefer to maintain their existing dividend levels and preserve more capital. UOB remains our preferred pick in the sector (BUY, TP S$29.20) as a defensive pick for its high dividend yield of c.4.7%.”

The research highlighted the following areas:

- Loan repricing continues into 2Q19; likely to still see marginal NIM improvement

- Apr-May’19 saw strong industry loan growth numbers amid slowing economy

- 2Q19 loan drawdowns likely to be on track with guidance

- Overall market sentiment remains resilient, supporting wealth management income

“According to our channel checks, repricing of loan book as well as mortgages are still ongoing in 2Q19 following that in 1Q19. While we are likely to still see marginal NIM improvement across the Singapore banks, we believe that OCBC’s NIM improvement in 2Q19 is unlikely to be as strong as that in 1Q19 (+4bps q-o-q) where the bulk of loan repricing was done. We believe that UOB is also likely to let go of some excess funds which have been weighing on its NIM in the last few quarters, and hence is likely to reverse the trend of NIM decline.

Singapore banks are due to declare interim dividends alongside 2Q19 results (DBS: 29 Jul 2019, OCBC and UOB: 2 Aug 2019). We believe that with the existing macroeconomic conditions alongside some market uncertainty, there is unlikely to be any upside surprises on dividends as banks would prefer to maintain their existing dividend levels and preserve more capital. UOB remains our preferred pick in the sector (BUY, TP S$29.20) as a defensive pick for its high dividend yield of c.4.7%.”

“Mortgages largely flat in May’19; limited growth upside expected for now. In May’19, mortgage book across Singapore was largely flat (-0.1% m-o-m; YTD -0.9%). As of 1Q19, mortgages represented 24% of Singapore banks’ total loan book.

While DBS Group Research does not expect the mortgage book to contract severely, unless there is an accelerated slowdown in the economy with massive unemployment, we believe that recovery in secondary sales transactions is needed to catalyse growth in mortgages, amidst a flattish primary sales environment.”

How to Secure a Home Loan Quickly

Are you planning to invest in properties like the collective sale relaunch site but ensure of funds availability for purchase? Don’t worry because iCompareLoan mortgage broker can set you up on a path that can get you a home loan in a quick and seamless manner.

Our brokers have close links with the best lenders in town and can help you compare Singapore home loans and settle for a package that best suits your home purchase needs. Find out money saving tips here.

Whether you are looking for a new home loan or to refinance, the Mortgage broker can help you get everything right from calculating mortgage repayment, comparing interest rates all through to securing the best home loans in Singapore. And the good thing is that all our services are free of charge. So it’s all worth it to secure a loan through us.

For advice on a new home loan.

For refinancing advice.