The local residential market appears to have shrugged off worries about the downbeat Singapore economic data lately, and staged a solid rebound in prices in the second quarter, demonstrating resilience in the underlying demand for the sector.

Cushman & Wakefield (C&W) which made this observation on the local residential market base on URA’s Q2 2019 statistics, said, “according to Q2 2019 URA data, overall private property prices rose 1.5% quarter-on-quarter (q-o-q), reversing losses in Q1 2019. Year-to-date (YTD), private property prices are up 0.8%. Gains were led by the non-landed segment, which rose 2.0% q-o-q. Landed prices saw a slight fall of 0.1% q-o-q.”

The rise in overall prices in the local residential market can be attributed to the continued take-ups for new launches on the back of a benign interest rate environment, stable job market and pent-up domestic demand, said C&W.

Table of Contents

There is little ambiguity about the lifting of cooling measures having prompted some buyers to come off from the sideline. Demand is now particularly sensitive to any shifts in price and quantum, given the tighter loan restrictions and higher Additional Buyer’s Stamp Duty (ABSD) following the July 6 cooling measures.

C&W said that the rise in prices in the local residential market was broad-based, with all 3 market segments increasing in Q2 2019. Rest of Central Region (RCR) prices rose the most, rising 3.5% q-o-q while Core Central Region(CCR) and Outside Central Region (OCR) prices rose 2.3% and 0.4% respectively.

“The RCR outperformed the rest of the segments, possibly because of the sales from new launches: there were a total of 1162 new sales in the RCR, out of 2350 total new sales, around 49.4% of total new sales in Q2 2019. Also, the encouraging performance of 2 recent freehold RCR launches namely, Amber Park and Sky Everton could have helped lift overall RCR prices. Amber Park and Sky Everton sold a total of 156 units ($2476 psf) and 131 units ($2524 psf) respectively, according to caveat data. The average new sale price for RCR in Q2 2019 was $1818 psf.

Although OCR prices underperformed the rest of the segments in Q2 2019, prices have reached a historical peak. Since the market recovery in Q3 2017 to Q2 2019, OCR prices have grown 11.7%. In comparison, CCR and RCR prices have only gained 7.5% and 11.5% respectively, over the same time period. OCR prices could still see further upside but growth is expected to be moderate.”

Liquidity from en bloc winners in the recent en bloc cycle is still expected to come into the market, supporting demand and property prices. Although the overall demand is still healthy, competitions are also rising as take-ups are also spread out among the numerous new launches across the island due to the spike in the pipeline.

Developers are refraining from any price cuts in the local residential market, in the short and medium term unless macro-economic conditions deteriorate further, said C&W.

There was a total of 2350 new sales in Q2 2019, bringing YTD new sales volume to 4188 units. We are cautiously optimistic that 2019’s sales could exceed 8,000 units, which is a marginal 10% moderation from 2018’s total sales.

“CCR prices gained 2.3% q-o-q in Q2 2019, clawing back some of the losses (-3% q-o-q) in 1Q19. Interest from overseas buyers particularly in the high-end segment seems to be sustained even post-cooling measures, further strengthening the appeal of Singapore property as an asset class.

In addition, the recent turmoil in Hong Kong and the United Kingdom due to the Hong Kong protests and Brexit could bode well for the residential market here, as high-net-worth-individuals start to eye on other wealth centres such as Singapore to preserve their wealth.

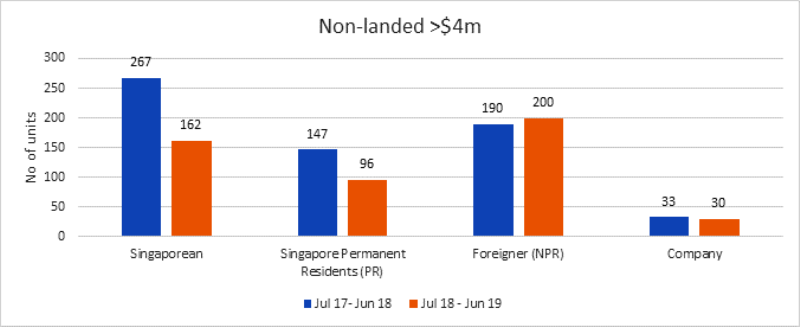

Nonetheless, geopolitical and trade tensions in the region have led to increased foreigner interest in Singapore properties. This is evidenced by the increase in foreigners buying non-landed properties above $4 million post cooling measures. Given the defensive nature of property, the inflow of funds could eventually lead to property investments in the city state.”

C&W observed that the unsold inventory in the local residential market came down slightly to 33,673 units, falling 5.4% q-o-q.

“Overall rents continue to edge higher on the back of low incoming completions. Non-landed rents rose 1.4% in Q2 2019. CCR, RCR and OCR rents rose 1.5%, 1.4%, and 1.2% respectively,” said Christine Li, C&W’s Head of Research for Singapore and SEA.

“The short to mid-term outlook for the rental market remains favourable, with the bulk of incoming completions expected to only enter the market in 2022 (18,885 units). The average annual completions over the last 10 years (2009-2018) is 14,211 units,” she added.

How to Secure a Home Loan Quickly

Are you planning to invest in properties but are ensure of funds availability for purchase? Don’t worry because iCompareLoan mortgage broker can set you up on a path that can get you a home loan in a quick and seamless manner. We are the experts who do the work for you for free, while you lean back, rest and rely on our professionalism at absolutely no cost to you.

Our brokers have close links with the best lenders in town and can help you compare Singapore home loans and settle for a package that best suits your home purchase needs. Find out money saving tips here.

Whether you are looking for a new home loan or to refinance, the Mortgage broker can help you get everything right from calculating mortgage repayment, comparing interest rates all through to securing the best home loans in Singapore. And the good thing is that all our services are free of charge. So it’s all worth it to secure a loan through us.

For advice on a new home loan.

For refinancing advice.