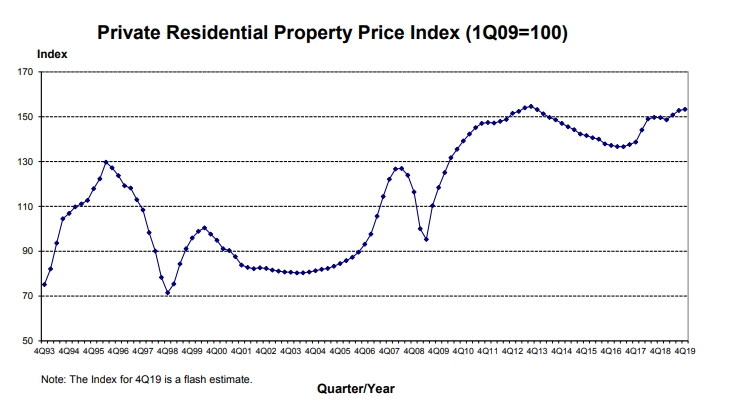

For the whole of 2019, private residential property prices have increased by 2.5%, compared to the 7.9% increase in 2018

The Urban Redevelopment Authority (URA) released the flash estimate of the price index for private residential property for 4th Quarter 2019 today. Overall, the private residential property index increased by 0.5 point from 152.8 points in 3rd Quarter 2019 to 153.3 points in 4th Quarter 2019. This represents an increase of 0.3%, compared to the 1.3% increase in the previous quarter.

For the whole of 2019, private residential property prices have increased by 2.5%, compared to the 7.9% increase in 2018.

For the whole of 2019, private residential property prices have increased by 2.5%, compared to the 7.9% increase in 2018.

Private residential property prices in CCR decreased

Prices of non-landed private residential properties decreased by 3.7% in Core Central Region (CCR), compared to the 2.0% increase in the previous quarter. Prices in the Rest of Central Region (RCR) decreased by 1.4%, after registering an increase of 1.3% in the previous quarter. Prices in Outside Central Region (OCR) increased by 2.9%, compared to the 0.8% increase in the previous quarter. For the whole of 2019, prices in CCR decreased by 2.6%, while prices in RCR and OCR increased by 2.7% and 4.3% respectively.

The flash estimates of the private residential property prices are compiled based on transaction prices given in contracts submitted for stamp duty payment and data on units sold by developers up till mid-December. The statistics will be updated on 23 January 2020 when URA releases its full set of real estate statistics for 4th Quarter 2019.

Past data of private residential property prices have shown that the difference between the quarterly price changes indicated by the flash estimate and the actual price changes could be significant when the change is small. The public is advised to interpret the flash estimates with caution.

Home ownership is ranked highly on many Singaporeans’ list of priorities, and private housing remains a longstanding aspirational goal, both for first-timers and HDB upgraders. The injection of ample supply in the last few quarters, provided home seekers with abundant options and in tandem with competitive pricing, outstanding design and good locational attributes, catalysed a substantial volume of conversion. private residential properties’ demand was project specific and uneven across the market.

Figures released by the URA last month showed that developers sold 1,147 new private homes (excluding Executive Condos) (ECs) in November 2019, rose by 23.2% from the restated 931 units transacted in the previous month, even as launches declined 17% MOM to 740 units.

On a year-on-year basis, new home sales were a slight decline of 4.5% from the 1,201 units shifted in November 2018, where there were eight new launches as sentiment recovered four months after the cooling measures in July 2018. November’s sales numbers took overall new home sales to 9,547 (excl. ECs) for the first 11 months of 2019 – up 10.2% from 8,662 units transacted over the same period in 2018.

Colliers Research projects that new home developers sold in 2019 will likely reach 10,000 units, surpassing the 8,795 units (excl. ECs) transacted last year.

It added that mixed residential developments took the limelight in November as Sengkang Grand Residences and One Holland Village Residences were among the top three best projects developers sold in November. Both also set benchmark prices for 99-year leasehold projects in their locality, reflecting good demand, despite a price premium, for well-located projects that also combine convenience and community.

The best selling private residential projects among units developers sold in November were: Sengkang Grand Residences which sold 235 units at a median price of SGD1,741 psf; Parc Esta which moved 102 units at a median price of SGD1,685 psf; One Holland Village Residences which transacted 87 units at a median price of SGD2,604 psf; Jadescape which shifted 60 units at a median price of SGD1,679 psf; and Parc Botannia which saw 59 units changed hands at a median price of SGD1,341 psf.

Top 10 Selling Projects in November 2019 (including EC)

| Project Name | Street Name | Locality | Units Sold in the Month | Median Price ($psf) in the Month | % sold to date (of total) |

| Sengkang Grand Residences | Compassvale Bow | OCR | 235 | 1,741 | 35% |

| Parc Esta | Sims Avenue | RCR | 102 | 1,685 | 69% |

| One Holland Village Residences | Holland Village Way | CCR | 87 | 2,604 | 29% |

| Jadescape | Shunfu Road | RCR | 60 | 1,679 | 45% |

| Parc Botannia | Fernvale Street | OCR | 59 | 1,341 | 94% |

| Treasure At Tampines | Tampines Lane | OCR | 48 | 1,377 | 39% |

| Parc Clematis | Jalan Lempeng | OCR | 36 | 1,600 | 34% |

| Affinity At Serangoon | Serangoon North Avenue 1 | OCR | 35 | 1,498 | 61% |

| Avenue South Residence | Silat Avenue | RCR | 35 | 2,000 | 40% |

| Dairy Farm Residences | Dairy Farm Lane | OCR | 35 | 1,564 | 8% |

Source: Colliers International, URA

5 new launches in November 2019

| Project Name | Street Name | Locality | Total Number of Units in Project | Units Launched in the Month | Units Sold in the Month | Median Price ($psf) in the Month | % sold (of launched) |

| Dairy Farm Residences | Dairy Farm Lane | OCR | 460 | 40 | 35 | 1,564 | 88% |

| One Holland Village Residences | Holland Village Way | CCR | 296 | 126 | 87 | 2,604 | 69% |

| Pullman Residences, Newton | Dunearn Road | CCR | 340 | 25 | 12 | 2,914 | 48% |

| Sengkang Grand Residences | Compassvale Bow | OCR | 680 | 280 | 235 | 1,741 | 84% |

| The Iveria | Kim Yam Road | CCR | 51 | 51 | 13 | 2,660 | 25% |

Source: Colliers International, URA

Ms Tricia Song, Head of Research for Colliers International Singapore, commenting on the units developers sold said: “Despite the global trade and geopolitical uncertainties, we believe demand for Singapore private homes is still relatively stable given the tight labour market, favourable interest rate environment, and relatively healthy household balance sheet.”

Private residential property prices are expected to continue to stabilise and rise by 2.5% for the full year 2019, said Colliers.

“Prices will likely be kept in check with the economic slowdown and an ample pipeline. As of end-November, there are also 4,323 private homes (excl. ECs) that have been launched but still unsold. December could see slower sales due to the festivities and holidays. We expect developer sales could touch 10,000, surpassing 2018’s 8,795, but still lower than 2017’s 10,566 units.

We estimate 2019 to have seen bumper new launches, with over 17,000 units in total among them. Takeup rates have been mixed, but we expect takeup to gradually improve over the next few years as the launch pipeline has peaked.

In 2020, we expect fewer new private residential launches of about 41 projects with 9,000 units in total, and barring a worse-than-expected economic slowdown, takeup should be similar to 2019 at 9,800 units. Prospective buyers would likely dip into earlier launches for choices. With a projected slightly better economic growth than 2019, we expect the private residential price index to grow 3%, in line with the economic growth.

Some of the largest launches in 2020 would probably be the most watched, these include: KI Residences (former Brookvale Park), 648 units; Leedon Green (former Tulip Garden), 638 units; and the Tan Quee Lan site, 580 units.”