Australia Property: Borrow in Singapore or Australia

Angeline C (iCompareLoan.com)

Australia is a popular investment destination among Singaporeans. And several banks in Singapore offer property investors an option to borrow, whether in SGD or a foreign currency.

If you have plans to buy a property in Australia, is it better to get a loan from a bank in Singapore or in Australia?

Pros of borrowing in Singapore

Banks in Singapore offer Singapore based investors the convenience of dealing with banks here and also perhaps a greater peace of mind when dealing with a bank you are familiar with and knowing that the bank is subject to strict regulations set by MAS.

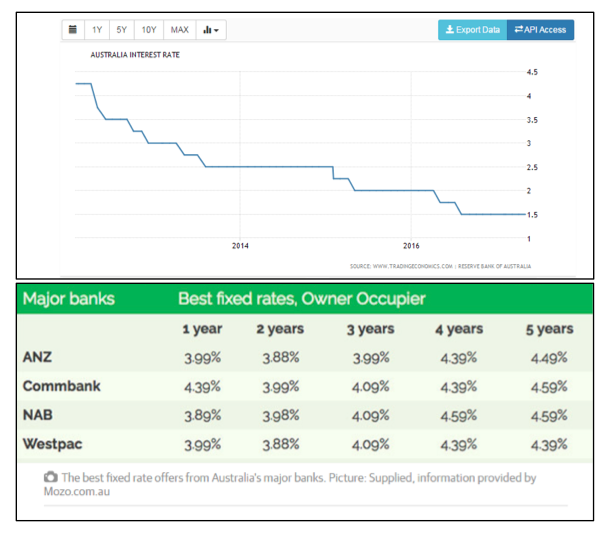

The interest rate offered are also typically lower. Loans offered by banks in Singapore are typically variable rate loans pegged to the SIBOR or board rate while lenders in Australia offer both fixed and variable rate loans (pegged to Reserve Bank of Australia rates). In recent months, the big four Australian banks, including Westpac and National Australia Bank were reported to have raised home loan interest rates for investor loans due to rising funding costs and greater regulation. In comparison, the rate from a lender in Singapore could be in the range of 3%. This is despite the fact that Australian cash interest rates are at a 5 year low of 1.5%.

Figure 1: Australia Interest Rate, Australian Property Loan rates by Major banks, Trading Economics, Reserve Bank of Australia, Mozo, Geelongadvertiser, iCompareLoan.com

In Singapore, borrowers have the option of a SGD or AUD or multi-currency loan but taking a non-AUD loan would involve forex risk since the property is denominated in AUD. This could subject the borrower to a margin call when the AUD depreciates against the base currency.

Eg: In 2014, Mr Lim bought an Australian property at A$900,000 and took up a loan of the Singapore dollar equivalent of A$630,000 (70% LTV). Assuming the exchange rate at A$/S$ = 1.15, the loan translates to S$724,000.

Now, the outstanding loan is S$800,000. Assuming an exchange rate of A$/S$ = 1.03, the loan is A$776,699 which represents a LTV of 86% assuming the valuation stays at A$900,000. This would trigger a top up to rebalance the LTV to 70%.

Cons of borrowing from a lender in Singapore

Taking a loan from a Singapore lender means it would be subject to MAS regulations such as the total debt servicing ratio or TDSR.

The maximum age limit is lower at up to 75 years for Singapore lenders vs 99 years in Australia.

The loan to valuation (LTV) will vary depending on whether you are an Australian citizen, permanent resident or non resident, self employed or hold temporary visa. It ranges from 70% at a Singapore lender to 80% at an Australian bank.

Singapore based banks offer only variable interest rates while banks in Australia offer the option of fixed and variable loans.

Banking fees are typically higher in Singapore.

Lenders in Singapore have restrictions on the location of your property, typically limited to Melbourne, Sydney and Perth.

Lenders in Singapore typically do not offer a deposit offset feature, ie interest owed on loan offset with the interest earned on a deposit whereas some Australian lenders do offer this feature.

The minimum loan is higher at S$300,000 for a Singapore lender vs A$100,000 for an Australian lender.

- Singapore lenders require the build in area of a property to be upwards of 50 sqm compared to a minimum of 40 sqm for Australian lenders.

- Singapore lenders also shun certain suburbs where it is more deemed less desirable or far from city centre, i.e. more than 5km radius away.

Legal fees and valuation fees are to be paid by the property buyer.

Hence do not get upset when we ask you for the Full property details and developer name. If you are unable to provide these information, we cannot proceed further.

Home Loan Rates for Singapore lenders For Australian Properties

Singapore lenders typically use 3 month Sibor + Spread for pricing the Australian properties. The lenders will lend you in Singapore dollars.

Documentation

Documents required are similar to that for Singapore home loans, with the usual being your pay slip, bank statement, passport and property purchase agreement.

Summary

It seems that there are more cons to pros when borrowing from a Singapore lender. But everyone’s situation is unique. Rumour has it that, getting an Australian Property Loan in Australia has become harder due to fraud by mortgage brokers (those who are Australian PR of Chinese nationality or Newly minted Australians who were formerly from China) in Australia who faked Chinese Citizen’s income documents. This led to wide spread tightening.

However at the time of publishing, Australian banks have tightened Non-resident lending. Hence it is now extremely hard to get a loan for Non australian residents within Australia. Although there are many reasons, part of the reason could be because Australian banks are slightly behind schedule for Basel III implementation.

For more information on this, you can contact a mortgage broker to help you in this process, click here.

If you do not wish to borrow for your australian properties, perhaps you could try for an Equity-term-loan in Singapore and pay your australian property in full.

If you are interested in finding more about home loans, click here https://www.icompareloan.com/resources/a-guide-to-housing-refinancing-in-singapore/

If you are interested in finding more about fixed vs floating rates, click here https://www.icompareloan.com/resources/fixed-rate-versus-floating-rate-home-loan-packages-in-singapore-which-is-right-for-you/

Image Credits: Eastern_Grey_Kangaroo_Young_Waiting, Wikimedia commons, Quartl,