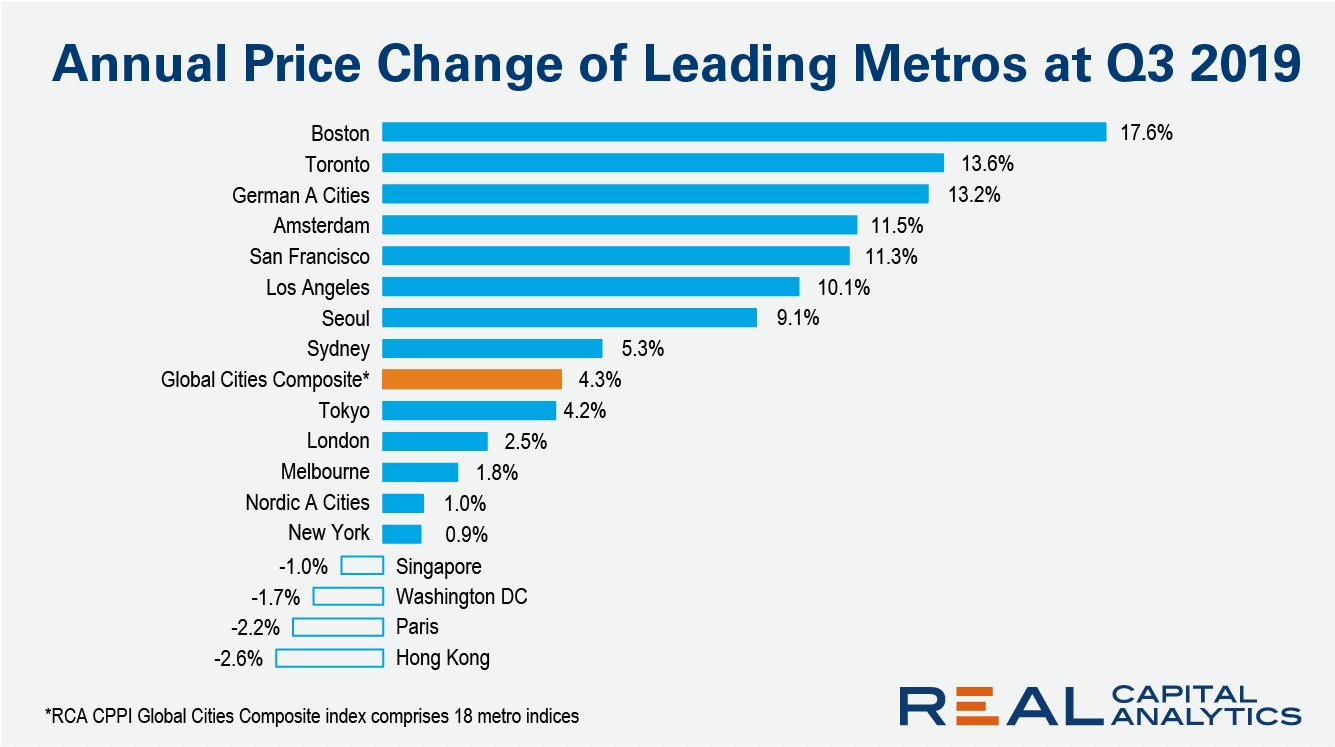

The pace of global commercial property price growth slowed further in the third quarter of 2019, reined in by weaker growth among metros in Europe and Asia, the latest RCA CPPI Global Cities report shows. The Global Cities Composite rose 4.3% from a year earlier, down from 6.4% at the start of 2019.

Annual price growth for global commercial property among the North American metros held at 6.7% in the third quarter, little changed over the course of 2019. For Europe, the composite price index slowed to a 4.2% year-over-year increase and the Asia Pacific index weakened to 2.0%, the slowest rate of annual growth since 2010.

Prices for global commercial properties in Boston grew the fastest in the third quarter, followed by Toronto and the German A Cities. Four metros posted outright declines; the steepest was troubled Hong Kong, where commercial prices dropped 2.6% from a year ago.

San Francisco, Boston and Los Angeles bucked the global commercial property trend of decelerating or falling commercial real estate prices at midyear 2019. Price growth in all three metros accelerated from a year earlier, with San Francisco posting price annual gains of close to 15%.

Amsterdam and Seoul were in the top five global cities for global commercial property price growth at midyear but price gains decelerated from a year earlier. Amsterdam is still posting quarterly price gains, but in Seoul prices dipped from the prior quarter.

Acquisitions of global commercial property dipped in the third quarter of 2019, with Europe and Asia Pacific leading the decline, the latest edition of Global Capital Trends shows. Activity in the U.S., which represents about one half of the global market for income-producing real estate, also weakened.

For the first nine months of the year, global trading of commercial property excluding land fell 7% from 2018. Among the world’s major country markets there were only a handful that posted an increase on 2018 levels, notably France and Singapore which have both benefited from cross-border investor interest. The U.K., Hong Kong and Canada all registered year-over-year declines greater than 30%.

U.S. commercial property prices rose 0.7% in September from August, maintaining the monthly pace of growth seen since May, the latest RCA CPPI summary report shows. The U.S. National All-Property Index rose 6.7% from a year ago.

There is wide variance in price trends across the individual property types. Apartment growth ticked up to an 0.8% monthly pace in September and quickened to a 7.7% annual rate, arresting the slowdown in price growth seen for this sector since early 2018.

The industrial index again posted the largest annual gain across the property types, up 11.9% YOY. Monthly price increases have slowed, however. Deal activity in the industrial sector climbed by 63% year-over-year in the third quarter of 2019, the latest edition of US Capital Trends shows, propelled by two giant portfolio transactions by Blackstone entities.

Price growth for both office and retail properties has softened significantly compared with the rates posted a year earlier. Office prices gained 3.1% year-over-year and retail prices only 1.4% year-over-year, the weakest rate for this sector since 2017. Deal activity in both these sectors was lower in the first nine months of 2019 compared to a year prior.

Liquidity is falling in more commercial real estate markets globally than it is growing for the second quarter in a row, the latest edition of the RCA Capital Liquidity Scores shows. The scores at midyear 2019 show a sharp division in the geographical distribution of the trend, however.

In the U.S., liquidity levels have grown due to elevated volumes through midyear and an increase in the buyer count. This trend is marked in the smaller markets, where increased interest from the major market makers and cross-border players has driven up liquidity.

In Europe, by contrast, the market has slowed in the first half of 2019 in response to political concerns, Germany’s lackluster economic growth and high prices in some core markets. Central London’s liquidity score dropped to the lowest level since 2009. In Asia Pacific, liquidity in Hong Kong, Australia’s core markets and all Japanese markets except Osaka declined.

European commercial property investment fell again in the second quarter of 2019, though the decline was shallower than that seen at the start of the year, the latest edition of Europe Capital Trends shows. The U.K. led the slowdown as deepening Brexit concern and retail sector woes dragged on investment activity.

Weakening economic sentiment, political uncertainty, high pricing, a shortage of suitable assets and structural shifts in demand have all contributed to the slowdown in European property investment through the first half of 2019. Total investment volume for Europe fell 10% year-over-year in the second quarter, compared with a 20% decline seen in the first quarter.

In the U.K., total acquisitions dropped by 46% year-over-year in the second quarter, making it the slowest three-month period for investment since 2012. For the first half of 2019, U.K. institutions spent more in continental Europe than at home.

The U.K. continues to be wracked with political uncertainty, which is negatively affecting commercial property deal flow and valuation indices. However, Real Capital Analytics analysis of transaction prices shows the right assets are still changing hands at elevated price levels.

U.K. commercial real estate transaction prices overall rose by 11.2% in Q1 2019 in comparison with a year earlier. This made the U.K. the best performer of all the country-level indices published by RCA.

The positive outturn might seem counterintuitive at a time of political flux and reduced transaction flow. However, the robust price trend illustrates that during times when there are few, if any, forced sellers in the market, it is the best quality properties that are finding a buyer.

Broadly, the academic research tells us that owners tend to sell winners and hold losers, and the current combination of political uncertainty, low volumes and rising prices supports tends to support that hypothesis. Owners also need an incentive to sell, given the cost of trading in and out of the market and the reported shortage of suitable assets for purchase. This also provides some of the impetus for prices to increase.