Association of Banks of Singapore (ABS) and Singapore Foreign Exchange Market Committee (SFEMC) proposals to improve the robustness of the market benchmarks and is calling for industry consultations and suggestions for improving the Sibor calculation methodology and scrapping the Sibor (12 month) due to lack of sufficient trading volume.

update 10th Dec 2017

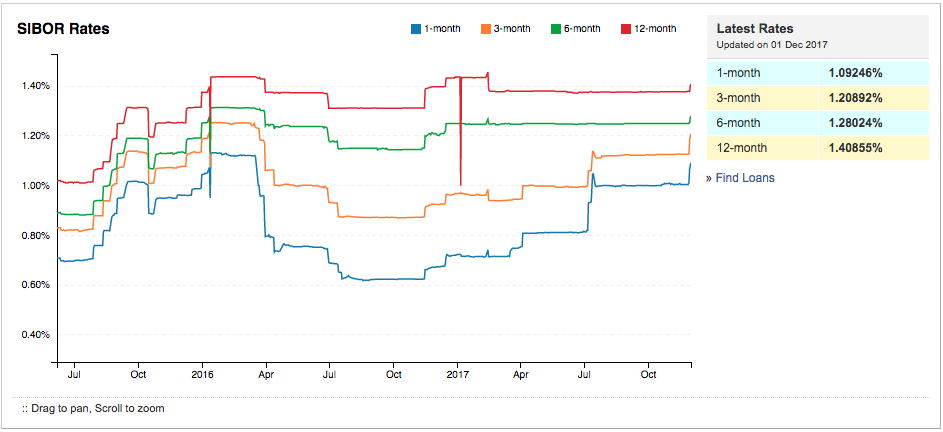

How much is Sibor Rate now?

Image Credits: Sibor Chart, ABS, iCompareLoan.com

Part of the reason for this review is due historically to LIBOR Rigging. As Libor is tied to almost US$350 trillion of derivatives, movement in Libor affects the pricing of these derivative financial products and billions could be made or lost due to Libor moves.

Sibor Is also rigged.

“The move comes a year after the MAS censured 20 banks in Singapore for trying to manipulate benchmark rates and ordered 19 of them to set aside reserves with the central bank — ranging from S$100 million to as much as S$1.2 billion each. The MAS found that 133 traders in the banks had tried to rig SIBOR, SOR, as well as foreign exchange benchmarks, although there was no conclusive finding that those attempts had succeeded.” (Today, 31st July 2014, https://www.todayonline.com/business/rate-rigging-be-criminal-offence-under-mas-proposed-law)

That makes is 20 out of 20 banks on the sibor reporting panel that is rigging the panel.

Sibor Reform What will it do?

The Sibor Reform will likely lead to Sibor being more widely used as a benchmark. This could cause the Sibor home loans to be more volatile for a period of time before stabilising. This could lead to momentary volatility in such home loans. In case you are worried, you can talk to a mortgage broker to assist you to switch out until there is more clarity on the situation about the Sibor reform.

Why LIBOR reporting Banks Lie?

Libor is measured via surveys to bank to ask them what they thought would be the cost of their borrowings had they gone to the market (with their partner banks) on the day itself. The data submitted is confidential.

During Financial crisis, banks lie and understated the rates they could borrow from the market had they gone to the market to borrow it.

This is because bankers do not truly believe that the rates submission is confidential and is symptomatic of the malaise of the financial industry. Banks who reported higher borrowing rates will be seen as being in a financially weak situation and will be shorted for profit and can easily lead to going belly up.

The reason is that LIBOR is a SURVEYED Benchmark, NOT an Actual transaction pricing, hence making rigging possible.

Voice recording – Interview with 938 NOW – on 5th Dec 2017 with Keith De Souza.

PLAY the Recording of the Interview with 938 NOW about the significance of the SIBOR.

Sibor is based on Actual transaction and is volume weighted and hence is in less risk of being rigged successfully. The only problem is when there is insufficient transaction data and there will be times when there is insufficient market transaction data leading to wild fluctuation of the SIBOR or other benchmarks. In such a scenario, how would SIBOR be robust enough?

If we were to base derivative and foreign exchange related derivative and interest rate derivative products, then the underlying benchmark that goes into the calculation or valuation needs to be robust and accurate.

This has massive positive potential for Singapore as a Financial Derivative market that as the potential to underwrite and issue hundreds of billions of dollars worth of derivatives. Imagine what kind of fees and charges and financial benefit the issuing banks could make.

How much derivatives are pegged to Sibor Benchmark?

There is no known amount of derivatives pegged to Sibor. As Singapore Dollar is not a major world currency, it is expected that Sibor is not used as a reference for too many financial products except mainly home loans in Singapore or for banks using Sibor as a property loan for overseas properties.

What is SIBOR?

Sibor is based on actual transacted data. Each day, at 11am The TOP 25% and BOTTOM 25% of the reported figures will be removed. The middle 50% of the data will be volume average weighted to reflect the SIBOR value. Hence for Sibor, there is not so much of an issue. There is no known data source to know how MUCH SIBOR is being used as a benchmark. You can read more about what is SIBOR and SOR here.

Sibor 1 month, 3 month and 6months are more widely used, however Sibor 12 months is hardly used. As a result, how do you calculate this benchmark, do we use a HYBRID of Survey as well as actual data to arrive at this figure?

Recommendations for Sibor Benchmarks

1. To introduce a money market exchange and settlement between banks to lend to each other. In this way, all transactions will be recorded and the rates and volume transacted will be transparent within the community. Of course not all banks will need funding everyday, hence a smaller volume, but with this, the doubt of rigging will be removed.

2. This could be enhanced together with calculation modifications. However a lot of home loan and other loan packages will be impacted.

APPENDIX: –

IOSCO

ABS Benchmarks Administration Co Pte Ltd (“ABS Co”) was subsequently set up in June 2013 to administer the Benchmarks. ABS Co is responsible to ensure the Benchmarks are representative, reliable, transparent and subject to a clear governance and accountability framework, in compliance with IOSCO’s Principles for Financial Benchmarks.1

Thomson Reuters – Calculation Agent for the Sibor and Sor benchmarks

LIBOR FRAUD – 27 July 2012 – Financial Times

“On 27 July 2012, the Financial Times published an article by a former trader which stated that Libor manipulation had been common since at least 1991.[8] Further reports on this have since come from the BBC[9][10] and Reuters.[11] On 28 November 2012, the Finance Committee of the Bundestag held a hearing to learn more about the issue.[12]”” (Wikipedia)

Libor FRAUD much earlier – 16 April 2008 – The Wall Street Journal

“On 16 April 2008, The Wall Street Journal released a controversial article, and later study, suggesting that some banks might have understated borrowing costs they reported for the Libor during the 2008 credit crunch that may have misled others about the financial position of these banks.” (Wikipedia)