Singaporeans are known to strive for high standards of living but is the Singapore system designed such that we have no choice but to upgrade all the time and end up with high cost of living? What if we are simple people and we really do not need to keep upgrading our lifestyle and are happy with simple lives?

You cannot lead a simple life even if you want to.

Image Credits: Building-under-construction, Nikman, Pixabay, iCompareLoan.com

Angeline C and Paul Ho November 2017

Let’s consider a young Singaporean looking to buy their first home. It is common advice to buy a HDB as your first home as it is significantly “subsidized” by the government as compared to private housing and there are grants that apply only first timers.

Example: Mr and Mrs Teo, both of whom are Singaporeans, with a combined income of $5,000 are applying for their first flat – a three bedroom flat in Geylang priced at S$380,000.

CPF grants which they are eligible for:

Additional Housing Grant: S$5,000

Special Housing Grant: S$40,000

Total CPF grants: S$45,000

Cost after CPF grant: S$335,000. (Is it CPF grant or HDB grant?)

This is definitely much more affordable than a similar sized condo at Geylang priced at more than double the new HDB flat.

The grants vary depending on your current financial situation and family nucleus. You can read more about CPF grants here.

This is well and good if the couple intends to stay there till they are old. But if you are thinking of selling after the minimum occupation period of five years then you would probably have no other option than to upgrade – to a bigger flat or private property.

Here we look at some issues faced by second-timers.

- Income ceiling

It is very likely that with inflation and salary increment, the couple would now no longer qualify to buy certain categories of public housing as their income have risen over the five years.

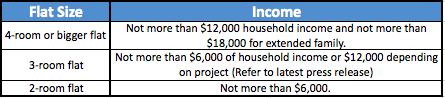

Currently, the income ceiling for a two room flat is S$6,000 as shown below.

- Buying a 4-Room or Bigger Flat – Not more than $12,000 household income and not more than $18,000 for extended family.

- 3-room flat – Not more than $6,000 of household income or $12,000 depending on project (Refer to latest press release)

- 2-room flat – Not more than $6,000.

Table 1: Income ceiling for Buying a flat from HDB for 2-room flat, 3-room flat and 4-room or bigger flat, HDB

Many young professionals you meet are already earning more than S$6,000 a month. What more for a couple, so they probably have to upgrade to a 4- or 5-room flat.

As you know, Singapore is a democratic country that behaves very much like a Managed economy while some communist countries are more capitalist in nature than Singapore. Singapore has strict categories for each group of people to fall into. Even if you want to be thrifty, you cannot! You are not allowed to be thrifty as that is not good for the economy.

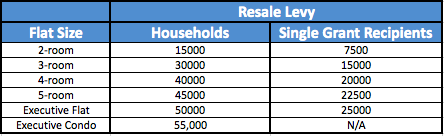

- Resale levy if you want to buy your second subsidized flat

If you sell your first subsidized flat for a second subsidized flat, you would need to pay a resale levy.

First Subsidised Housing Flat Types

- 2-room = $15,000 (Households); $7,500 (Singles Grant Recipients)

- 3-room = $30,000 (Households); $15,000 (Singles Grant Recipients)

- 4-room = $40,000 (Households); $20,000 (Singles Grant Recipients)

- 5-room = $45,000 (Households); $22,500 (Singles Grant Recipients)

- Executive Flat = $50,000 (Households), $25,000 (Singles Grant Recipients)

- Executive Condominium = $55,000; Not Applicable.

(Table 2: Household and Singles Grant Recipients Resale Levy Amount for different First Subsidised Housing Type, HDB)

For example, the Teos will need to pay a resale levy of S$30,000 if they wish to sell their current three room flat to buy a new four room flat.

This does not apply if the Teos buy a resale flat or private property.

This is still manageable but for the older generation who bought their first home before 3 March 2006 and are looking to downgrade to a smaller home for retirement, the resale levy can go up to over S$100,000!!

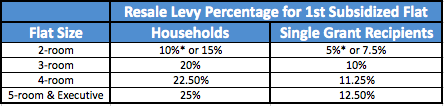

Resale Levy Amount: First Subsidised flat sold before 3 March 2006

Resale Levy amount for First Subsidised Flat Type: –

- 2-room = 10%* or 15% (Households); 5%* or 7.5% (Singles Grant Recipients)

- 3-room = 20% (Households); 10% (Singles Grant Recipients)

- 4-room = 22.5% (Households); 11.25% (Singles Grant Recipients)

- 5-room and Executive = 25% (Households); 12.5% (Singles Grant Recipients)

(Table 3: Resale Levy amount: First subsidised flat sold before 3 march 2006, HDB)

If you have not paid the levy when you sold your first flat, and deferred payment until you purchased another flat, an interest of 5% p.a. is charged!

Let’s look at a real-life example faced by Straits Times reader Madam Liu. This was in 2015. http://www.straitstimes.com/forum/letters-on-the-web/review-hdb-resale-levy-policy.

Basically, Mdm Liu said that the high resale levy made it difficult for her to downgrade to a BTO flat just as she was reaching retirement age.

She had bought her first HDB – a four room flat and upgraded to a five-room flat to accommodate her growing family in 1997.

She later learnt the total resale levy payable amounted to S$193,000! This comprised S$91,350 (22.5% of the resale price of her first flat sale in December 1997) and accrued interest (5%).

She is not alone. Many who are in their retirement are faced with this situation of being faced with exorbitant resale levy and are at a disadvantage of this two-tier system for calculation of resale levy.

As another ST reader says,” Paying a levy when one buys a second new flat directly from the HDB is equitable, but paying four times the amount, with interest continuing to accrue until a second purchase is done, seems rather unfair.” (http://www.straitstimes.com/forum/letters-in-print/have-uniform-hdb-levy-for-second-bto-flat-purchase)

HDB’s responded that the accrued interest will be waived for those who meet certain conditions –e.g. aged 55 and above, etc. (http://www.straitstimes.com/forum/letters-in-print/fairer-distribution-of-subsidies-through-resale-levy)

But still the question is why the two-tier system continues to exist.

- Second-timers not eligible for CPF Housing Grant

A flat may no longer be as cheap for second-timers as they are not eligible for CPF Housing grant, Additional Housing Grant and Special Housing grant. The grants can be quite substantial and help in subsidizing a home going up to S$80,000 for low income households.

So, for second-timers considering a new home, the decision may tilt more towards resale and private property as the price difference between a new flat and alternatives is lower.

- Quota for second timers

HDB gives priority to households buying their first homes. So for second timers, buying another flat from HDB is like striking lottery as the current quota is very low.

For second-time applicants of 2- and 3-room BTO flats, the quota is 15% for a flat in a non-mature estate and 5% for a flat in a mature estate. The second-timer quota for 4- and 5-room flats in non-mature estates is at 15%.

Conclusion

If you are thinking of selling your flat and buying a smaller flat from HDB, you could soon realise that you would face a roadblock at every turn, leaving you frustrated and helpless.

And yet your current finances may not allow you to go for resale and private property.

Next time when Singaporeans complain about HIGH COST OF LIVING, please do not BLAME Singaporeans that we aspire to COST OF HIGH LIVING and hence the high cost. Of course there are many reckless Singaporeans who spend beyond their means, but there are also many Singaporeans who actually are thrifty and do not need expensive Condominiums but are forced to upgrade.

If you are intending to sell your HDB to buy condo, there are also pitfalls to avoid. Talk to a mortgage broker to work out your home loan financing if you are considering selling your flat and moving to your next home or simply use the expert panel of agents selected by iCompareLoan.com who can assist you to manage the timing of selling and buying.

To read up more on property buying in Singapore, please click here or click here for the Ultimate Guide on Property Buying in Singapore.