APAC real estate investment volumes down by 27 per cent year-on-year, but pricing remains relatively stable with limited signs of distress

- rapid improvements in sentiment and investment appetite seen in key Asian markets since H1

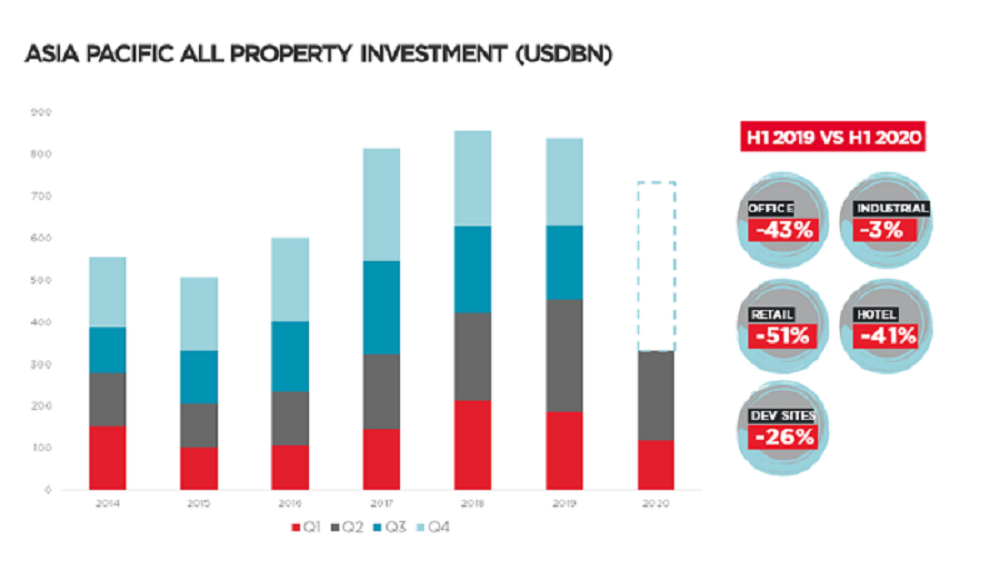

The overall regional real estate investment volumes were down by almost 40 per cent y-o-y in Q1 2020 at US$119bn – the softest quarter since Q1 2016. On the positive side, volume picked up in Q2 2020 to reach over US$200bn, however, this is below the three-year rolling quarterly average of US$209bn. The implication is that investment in 2020 is likely to fall well below last year’s totals.

Key cities such as Shanghai, Beijing, Seoul, and Tokyo saw activity through H1 202 and seem set to see ongoing activity in the second half.

At the sector level, investment in all asset classes is well below rolling averages, although investment in the retail and hotel sectors have been hard hit with both recording anemic volumes in H1 2020 – down 52 per cent and 41 per cent y-o-y respectively. There is limited interest in Retail or Hospitality assets, except in the case of retail where they play to the underlying daily needs of consumers. More broadly, these two asset classes will attract capital if there is repositioning potential or the possibility of a major adjustment in pricing.

Office investment also weakened dramatically, down 43 per cent, to $27bn. In contrast, the logistics sector continues to gain from the growth of ecommerce and has seen sustained investor interest and while down year-on year, the decline has been less dramatic than in other sectors at 3 per cent for H1 2020, which could also be more a product of a shortage of supply than an outright fall in demand.

Deployment of capital, of which there remains an abundance, is likely to remain challenging, although there is some encouraging activity in participation via clubs, joint ventures and partnerships. This may include follow on investments with managers and operators where the relationship was formed pre-COVID-19 where the need to travel to consolidate or cement the relationship is not as essential.

Dennis Yeo, Head of Investor Services, APAC said “Funds are actively deploying capital into development sites in the Southeast Asian markets of Indonesia, Vietnam, Philippines and Thailand, looking to gain a first mover advantage against the shortage of investment-grade logistics assets in these developing countries. Logistics players and REITs including LOGOS, ESR are actively seeking development opportunities to bolster their portfolios in the region. India’s REITs market continues to attract capital, which will then shore up its stock of trophy assets. In markets like Singapore, Tokyo and Seoul where core assets are tightly held, prices remain firm with owners appearing to have the upper hand.”

Transaction activity in the investment market is expected to improve in H2 2020 but will remain below trend despite limited signs of distress so far. With China showing early signs of a rapid rebound and the rest of the region set to follow suit towards the end of the year or early next year, the Asia Pacific region is proving to be particularly attractive to global investors, especially in mainstream sectors such as office and logistics as well as growing subsectors such as data centers and senior living. While a full recovery is still some way off, volumes would have likely troughed and should gain momentum in the latter part of the year.

“Investors have remained on the sidelines for much of H1 2020, with volumes down 27% year-on-year. As economies reopen, investment activity is expected to increase. Logistics appetite continues unabated and there is heightened interest in alternative asset classes. We are also experiencing ongoing interest in the office sector, albeit generally for lower risk stabilized assets in CBD areas.” said Gordon Marsden, Regional Director, Asia Pacific Capital Markets at Cushman & Wakefield.

- Carefully think whether to surrender/sub-lease space.

- Markets are likely to be flush with options resulting in low returns for sub-lessors.

- Align financial goals with CRE strategy, flexible working policies and change management to enact workplace transformation.

- Give high priority to office workplace design, technology, wellness and well being.

- Ensure facilities management is increasingly nimble and more focused on user experience than tactical delivery

- Prioritise wellness standards and touchless technology which are expected to increase in importance.

During the first half of 2020, we saw the pandemic have a material and unprecedented impact on the global economy, which has significantly disrupted commercial real estate around the world. Over the last quarter, countries across Asia Pacific have taken small steps towards recovery, with the region well placed to lead the world out of recession.

In its report Colliers International tool a look at where those green shoots of opportunity are emerging, their view on the second half of the year and how investors, landlords, and tenants alike should make real estate decisions in this environment.

Although real estate investment volumes in Asia Pacific were down in H1 by 42% year-on-year, pricing has remained relatively stable with limited signs of distress so far.

With activity expected to improve real estate investment volumes into H2, Colliers International expects to see investors:

- Work closely with lenders to maintain debt levels and where possible secure lending for new investment opportunities.

- Safeguard portfolio occupancy with new leasing and tenant retention becoming imperative.

- Accelerate development opportunities in logistics and warehousing led by rising occupier demand.

- Proactively seek sale-and-leaseback opportunities.

- Keep a close focus on price softening on pre-distressed assets or where existing owners need to rebalance their portfolio.