The Urban Redevelopment Authority (URA) today released the flash estimate of the price index for private residential property for 2nd Quarter 2018 which suggests that property price momentum here remains buoyant.

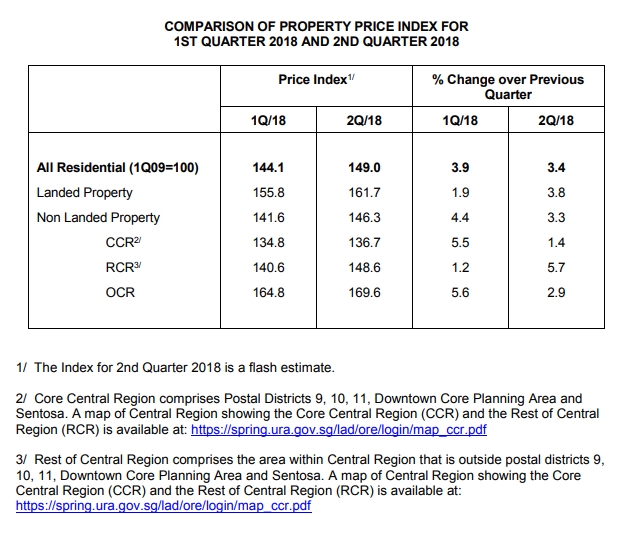

Overall, the private residential property index increased 4.9 points from 144.1 points in 1st Quarter 2018 to 149.0 points in 2nd Quarter 2018. This represents an increase of 3.4%, compared to the 3.9% increase in the previous quarter.

Prices of non-landed private residential properties increased by 1.4% in Core Central Region (CCR), compared to the 5.5% increase in the previous quarter. Prices in the Rest of Central Region (RCR) increased by 5.7%, after registering an increase of 1.2% in the previous quarter.

Property prices in Outside Central Region (OCR) increased by 2.9%, after registering a 5.6% increase in the previous quarter.

The flash estimates are compiled based on transaction prices given in contracts submitted for stamp duty payment and data on units sold by developers up till mid-June. The statistics will be updated on 27 July 2018 when URA releases its full set of real estate statistics for 2nd Quarter 2018. Past data have shown that the difference between the quarterly price changes indicated by the flash estimate and the actual price changes could be significant when the change is small. URA advised the public to interpret the flash estimates with caution.

JLL. a leading real estate consultancy firm, noted that URA’s private residential property price index rose 3.4% in 2Q18 (slightly lower than the 3.9% in 1Q18) but still reflective of the buoyant property price momentum in the market.

Table of Contents

It said that the property price increase in the second quarter was underpinned by increased new launches with strong pricing as well as increased volume of transactions. 11 new launches were recorded in 2Q18 as against 7 in 1Q18 while transaction volume based on caveats recorded rose 14.2% in the second quarter (to-date). New sales volume rose an estimated 48% while resale and sub-sale volume remained roughly flat in the second quarter.

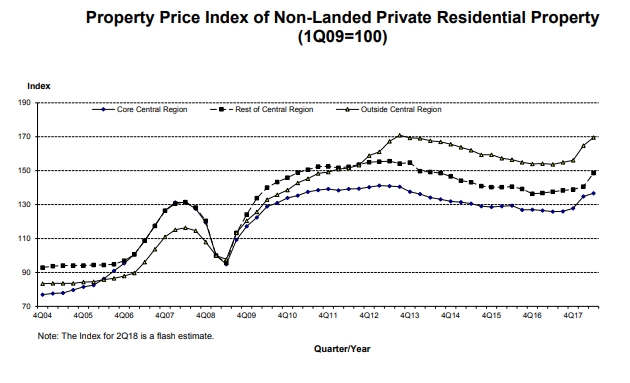

The Rest of the Central Region (RCR) spearheaded the non-landed price index increases in 2Q18 jumping 5.7%, from a gradual 1.2% in the first quarter. New launches with optimistic pricing contributed to the strong price increase in RCR. Examples of these new launches and their median prices include Amber 45 ($2,378 psf), Park Place Residences at PLQ ($2,045 psf), Margaret Ville ($1,871 psf), The Verandah Residences ($1,839 psf) and Harbour View Gardens ($1,763 psf).

The transaction volume in RCR rose 34.2% in 2Q18 (based on caveats recorded to-date) while the overall median price of $1,665 psf during the quarter was 12.7% higher than that in 1Q18. In 2Q18, new sales in the RCR non-landed market accounted for 45.8% of its transaction volume, significantly higher than 31.7% in the first quarter.

In the Core Central Region (CCR), prices increased at a slower pace in the second quarter as seen in the 1.4% rise in the non-landed price index, which is much lower than the 5.5% recorded in 1Q18. There were less new launches in CCR in 2Q18 while a few new launches in 1Q18, including New Futura, had already set a high base on pricing for new sales.

The non-landed price index for Outside Central Region (OCR) also recorded a lower increase of 2.9% in 2Q18, following a more significant rise of 5.6% in the previous quarter. The transaction volume of non-landed homes in OCR rose 12.7% in 2Q18 spearheaded by a 38.6% surge in new sales. Examples of new launches contributing to the non-landed price increase in 2Q18 in OCR include Twin Vew, Affinity at Serangoon and The Garden Residences. Previously launched projects such as The Tapestry, Kingsford Waterbay and Parc Botannia also recorded strong sales in the second quarter.

The landed price index strengthened 3.8% in 2Q18, a firmer pick-up from the 1.9% rise in the first quarter. Landed prices had fallen more substantially than non-landed between 2013 and 2017 and its price increase during this recovery cycle has lagged non-landed properties. As landed prices appear attractive, buyers have been drawn to the landed market contributing to the firmer price increase.

Mr Paul Ho, the chief mortgage consultant at icompareloan.com, agrees with JLL that the landed market should be attractive to home-hunters and investors going forward. He believes that as the sales proceeds start to come in from the en bloc sales completion from now till 2019, landed properties, especially the inter-terrace segment will pick up steam.

This Mr Ho said is because en bloc sales homeowners who are flush with cash, will resort to value hunting instead of choosing smaller condominiums which are beginning to sell at unbelievable prices. He also believes that the upward trend in the property price of non landed market is in its early stages and so is sustainable.

Mr Ho attributes the bullish non landed property market to the recent en bloc activities, which has seen a record number of en bloc collective sales of older condominiums. “This has led the property sellers to ask for higher selling prices,” he noted.

But such upward price surge for non landed properties may not hold true for cheaper estates or districts as they will have lesser branding for developers to do their markups. A traditionally non-luxury district will not be able to command a similar price premium regardless of how much the developer bought the land for.

If you are home-hunting, our Panel of Property agents and the mortgage consultants at icompareloan.com can help you with affordability assessment and promotional loans. The services of our mortgage loan experts are free. Our analysis will give industrial property loan seekers better ease of mind on interest rate volatility and repayments.

Just email our chief mortgage consultant, Paul Ho, with your name, email and phone number at paul@icompareloan.com for a free assessment.